Fund managers tend to generate a large part of their total compensation in the form of bonuses. This incentive-driven compensation can theoretically backfire if it induces fund managers to take excessive risks, but a survey of Norwegian fund managers indicates that this is not the case in practice.

Admittedly, the survey tracks only 37 fund managers from 2011 to 2015 and is thus low-powered, but it can give asset managers and asset management firms an indication of how incentives work in the industry.

The advantage of the survey was that it had access to the detailed incentive structures in 12 Norwegian asset management firms and the detailed performance and portfolio holdings of the 37 fund managers that responded to the study throughout the entire observation period.

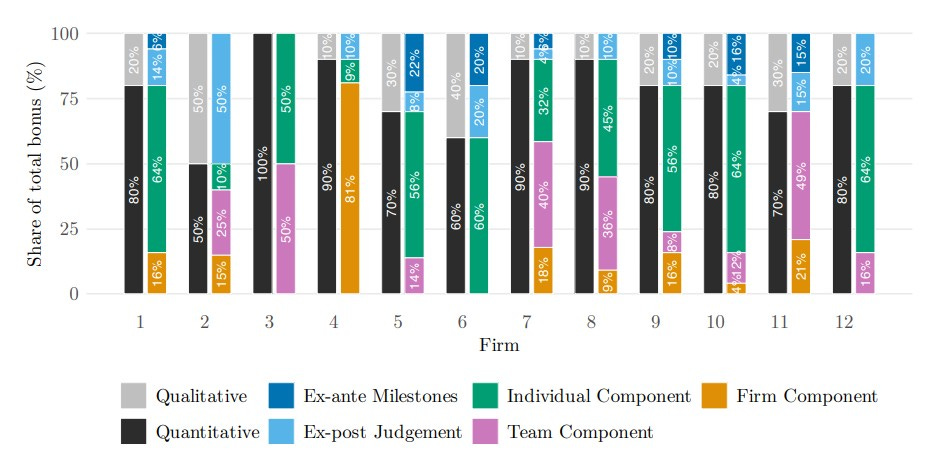

The chart below shows that almost all firms use a combination of quantitative and qualitative criteria. The quantitative criteria are usually based on the information ratio of the fund, i.e. the risk-adjusted performance vs. the benchmark rather than the raw performance difference between fund and benchmark.

Incentive structure at Norwegian asset management firms

Source: Bienz et al. (2025)

This obviously reflects an attempt to reduce the incentive for excessive risk-taking. If a fund manager is solely measured by the raw performance vs. the benchmark, the manager could simply gamble and take large risks. If the risks lead to strong performance, the upside for the fund manager is enormous, but if the fund implodes, the worst that can happen to the fund manager is to lose their bonus (and in the long run, their job), while investors may lose all of their money.

It’s basically the Cathie Wood school of fund management. Bet everything on a handful of stocks and hope it works out. If you are lucky, you gather extreme amounts of money from credulous investors and when the performance tanks afterward, you become the world’s largest wealth-destroying fund.

Additionally, fund management firms add qualitative criteria to the incentive structure (typically these qualitative criteria account for c.20% of the bonus determination), which focus mostly on teamwork, professional development, compliance, etc.

And it turns out that these bonuses work. Indeed, fund managers who can earn higher bonuses tend to perform better than fund managers with a smaller bonus pool. Crucially, this relationship between the size of the bonus and performance is almost entirely driven by the quantitative component. If you give fund managers larger incentives to perform well (while limiting excessive risk-taking), you get better performance. Furthermore, the fund managers in the survey did not increase risks in their portfolios when they had the opportunity to earn larger bonuses.

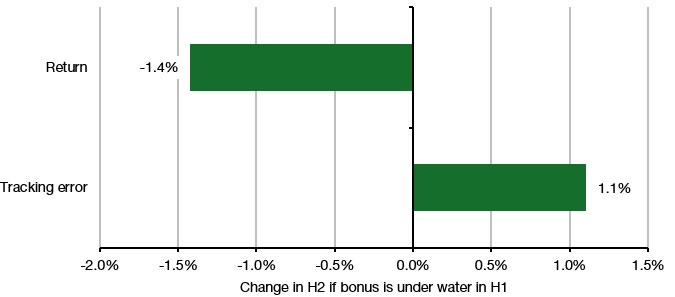

But they did increase the active risk in their portfolios when they were ‘under water’ in their mid-year reviews. The chart below shows that if a fund manager was at risk of missing their bonus targets in the middle of a calendar year, they tended to increase active risk (tracking error) in the second half of the year. Unfortunately, this increased risk typically does not pay off and returns vs. benchmarks declined even faster, creating a drag on the information ratio.

What happens if a fund manager is underwater in the middle of the year?

Source: Bienz et al. (2025)

It all boils down to the old adage that incentives matter and fund managers, just like most people, will adjust their behaviour in reaction to the incentives they encounter. Get the incentive structure right, and you encourage better performance. This survey indicates that Norwegian fund managers do indeed face the right incentive structure.