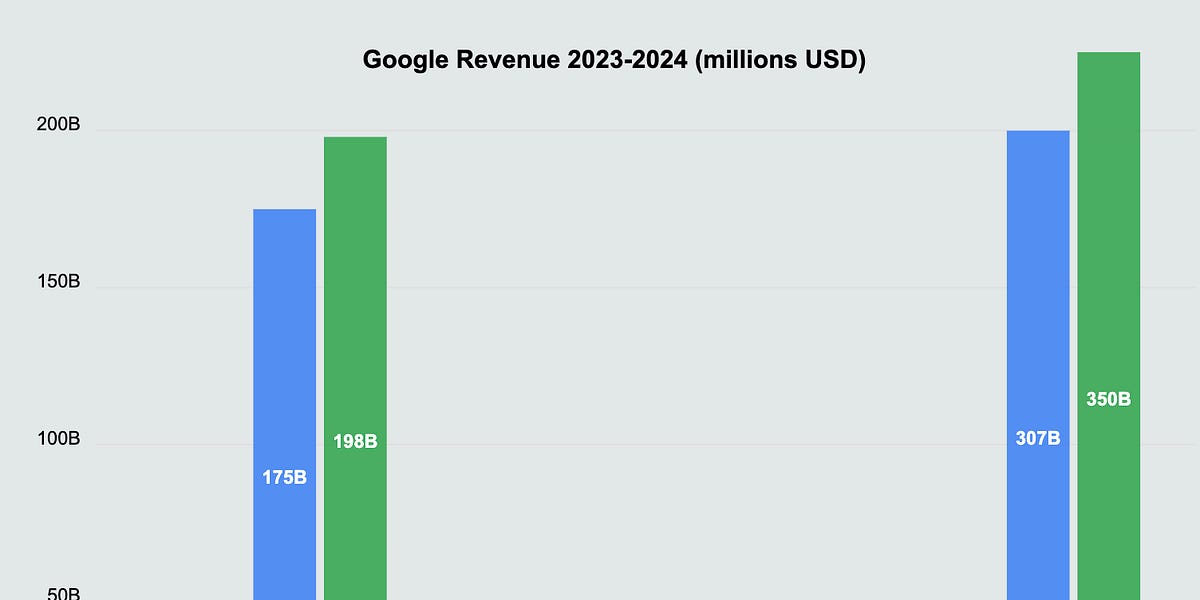

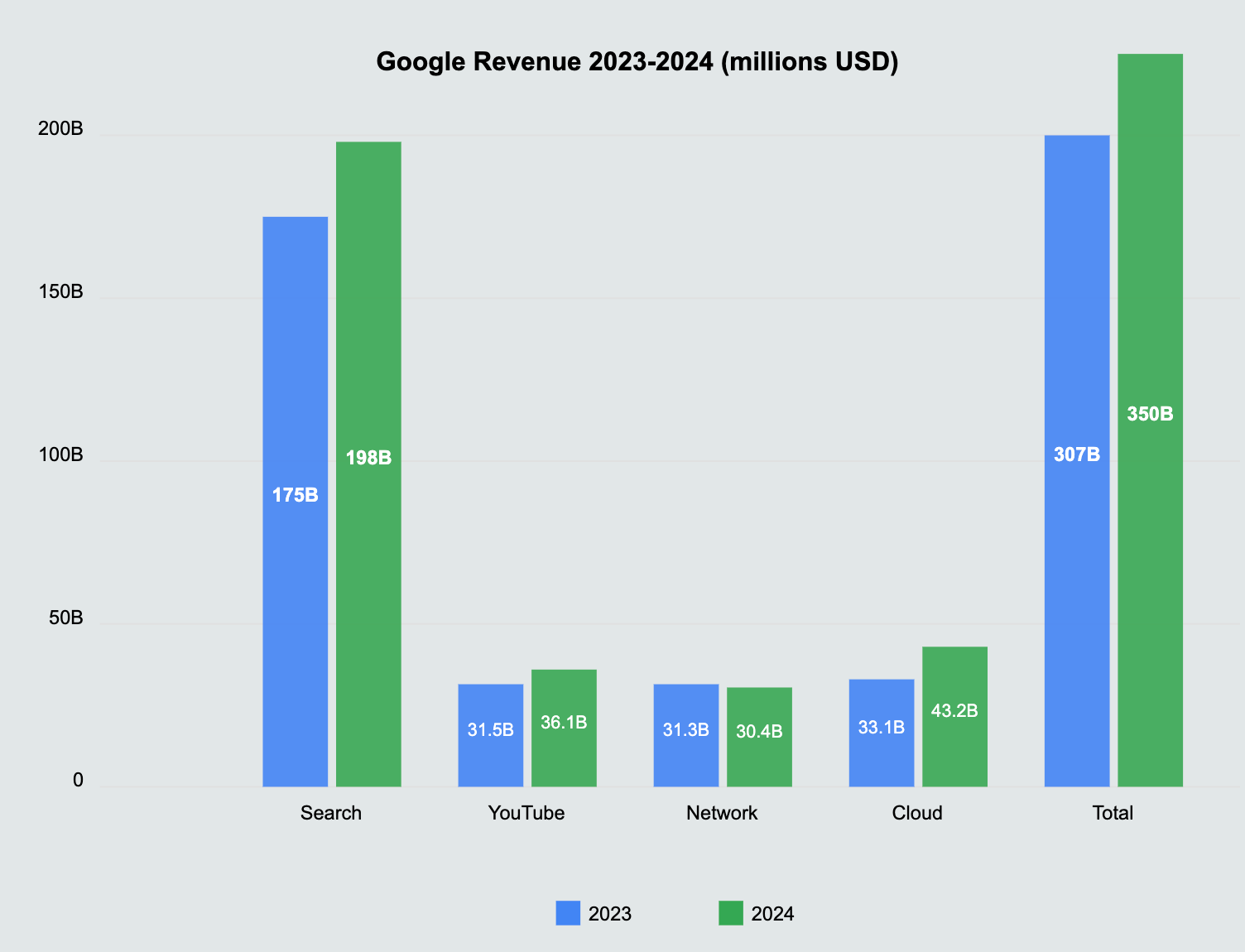

Google is a $350 billion yearly run rate machine, now in the AI business.

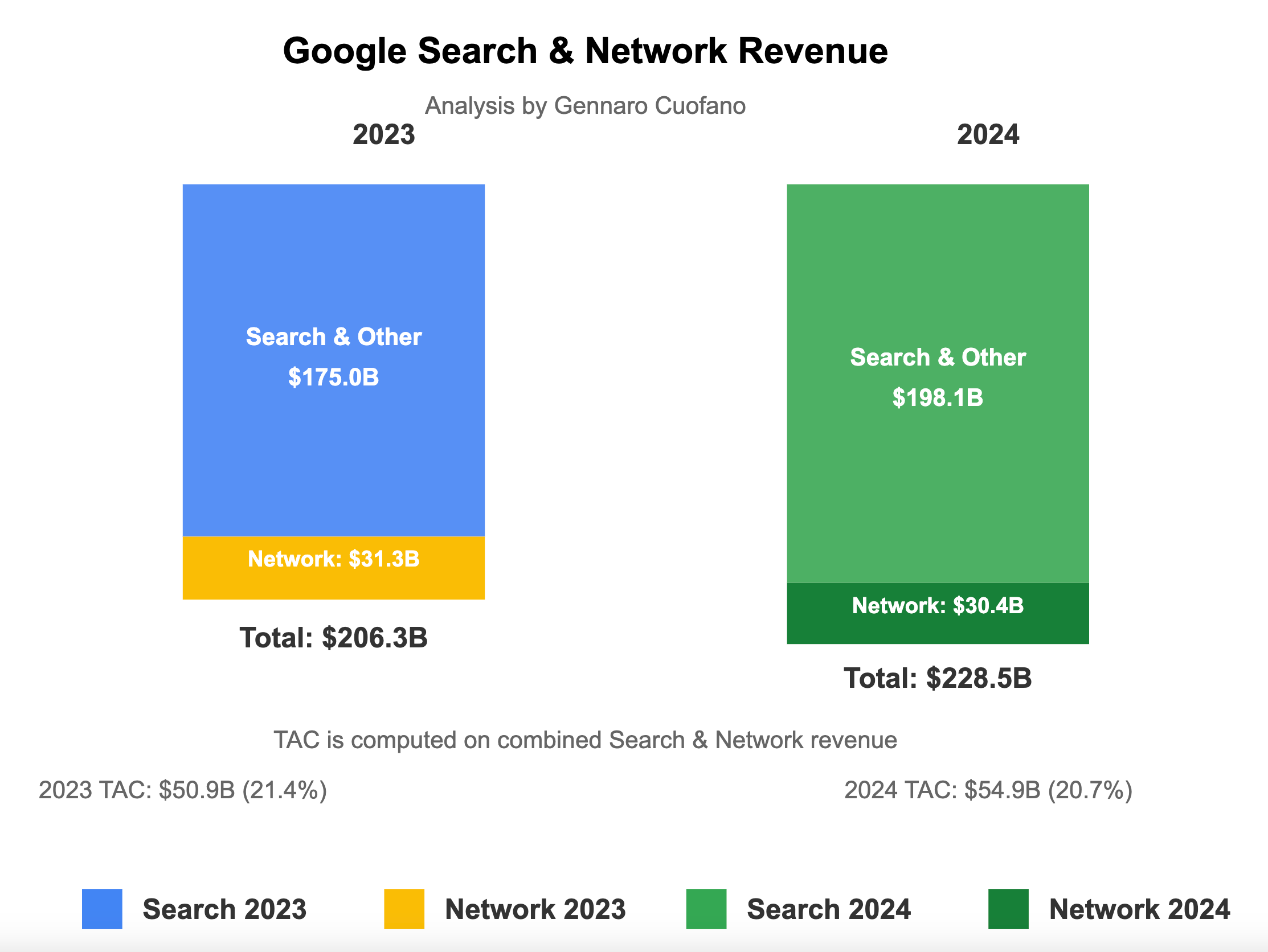

The key thing about Google’s search machine is that the company has managed to lower the cost of running a query while simultaneously making many times over it.

Google is now integrating AI into its core in two ways:

-

Google Search, with interfaces like AI Overviews in Search, has just expanded to 100+ countries, increasing search engagement, especially among younger users.

-

Google Ads Machine, with Google integrating AI features, from image generation to targeting, to improve the delivery and reach of these formats.

It means that with this simple AI integration, one on Google Search can at least try to patch things up in the short term, as redefining the whole search UX for AI at Google’s scale is (almost) mission impossible.

On the Google Ads side, the company can boost advertising budgets through it, thus translating these AI enhancements as a revenue leg up.

With the premise that Google Search might lose scale, advertisers might opt for other platforms.

Yet, a key advantage for Google is it also owns YouTube, which is probably still the most impressive digital platform.

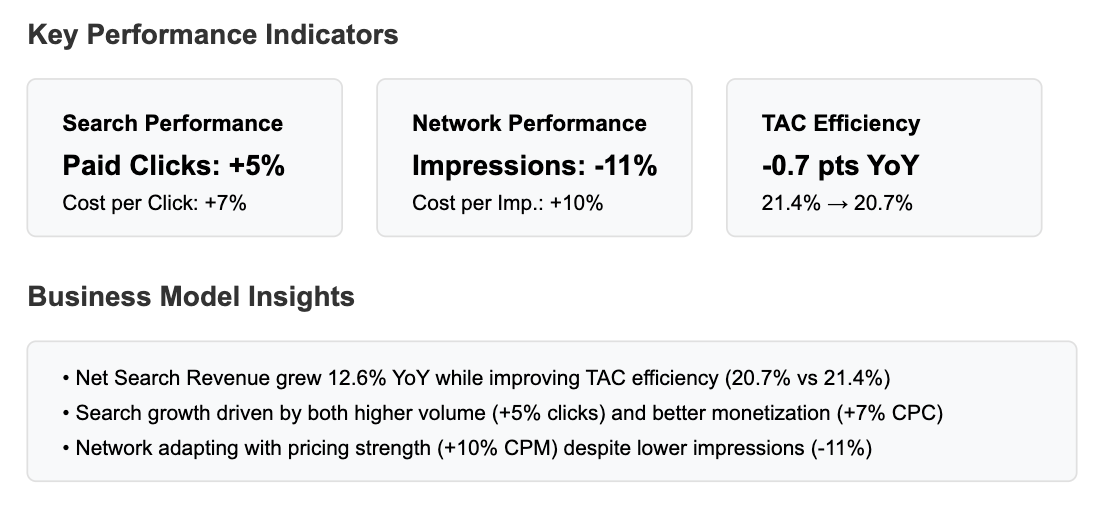

With the integration of AI into its Ad Machine, for instance, Google has seen improved search performance, which has also driven the cost per click higher, thus probably making the company a few more billion a year.

Thus, Google’s core moat is the search business.

And yet, the company has to defend it while attacking the AI side and transform-create on new AI-native lines of business.

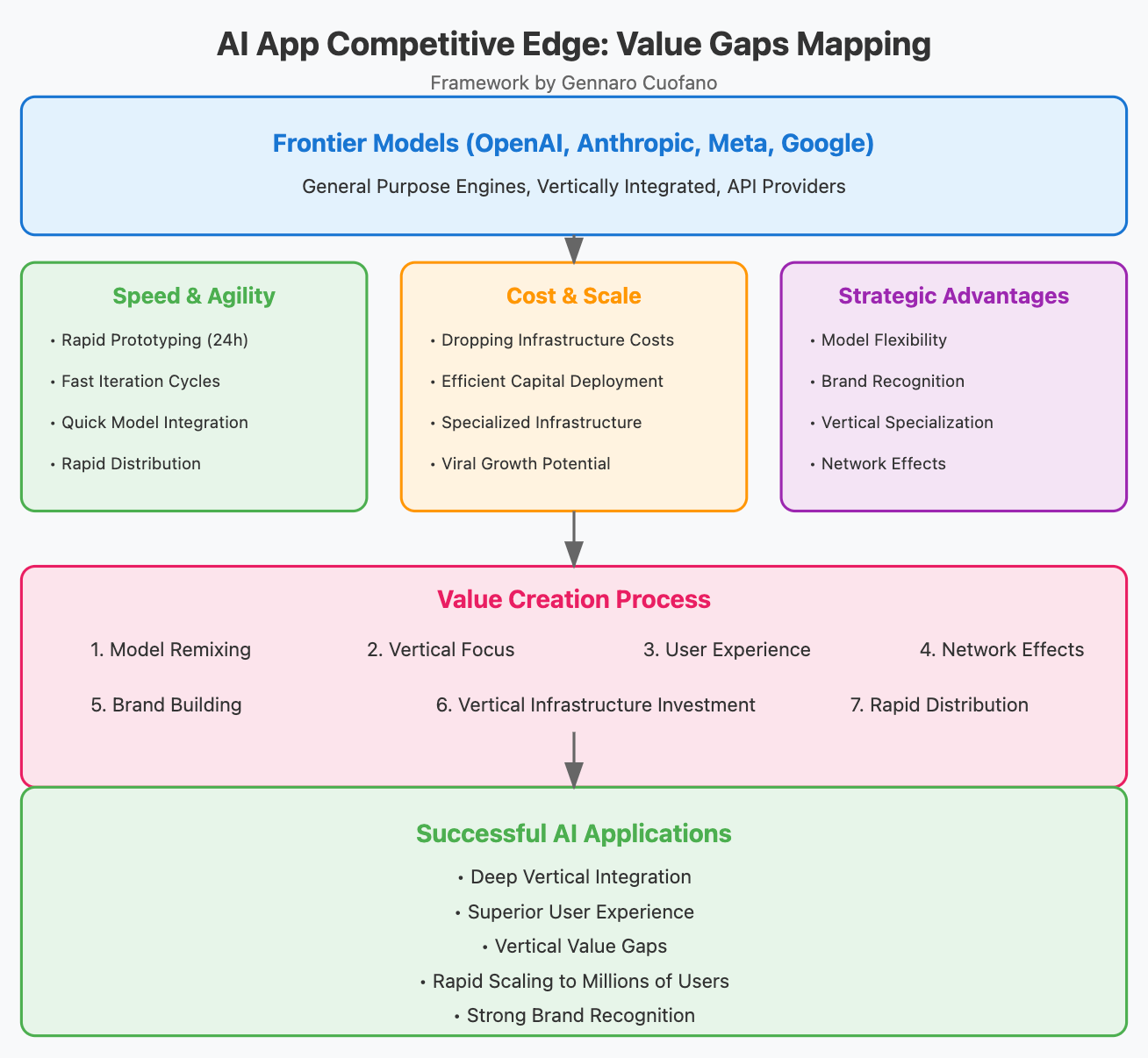

In this part, I’ll tackle what it means to build AI moats, if you’re operating outside the “frontier models landscape” (as it is for the majority of startups/companies out there).

That implies I’ll leave out, for now, a good chunk of the core ecosystem (frontier models, cloud infrastructures, and hardware), as I’ll tackle it in a separate issue.

I analyzed the AI landscape in December 2022 and developed a framework to understand how to build competitive moats in the new AI paradigm.

Below is my perspective, with a few minor updates based on current developments.

I’ll use this as a starting point to develop from there.

As soon as I saw ChatGPT at the end of November 2022, I deeply considered the nature of competition (as it developed) in the AI industry.

I wrote the below in late December 2022, and I think it gets confirmed more and more each day as the AI industry develops.

I’ve added a few more points and paragraphs based on current developments, but today’s main question remains.

Indeed, the main question that kept popping up in my head was: If we all build tools on top of ChatGPT/OpenAI or a few similar models, how can we build competitive moats?

In other words, how can we build a company on top of AI with a long-term advantage that cannot be easily commoditized?

And just like two years back, my answer is the same, and it can be summarized as you can absolutely build AI Moats even if you’re not operating at the foundational layer!

I think there are a few things to take into account here.

As we went along this intense journey, where nearly two years have seemed a decade, what I’ll explain below has actually been confirmed.

We saw the emergence of startups like Perplexity AI – outside pure foundational players like OpenAI, who will need to spend billions on infrastructure alone – becoming valuable companies.

In reality, as I’ll explain below, valuable companies will emerge in each layer of the AI industry, but each layer will have a completely different logic.

Let me explain!

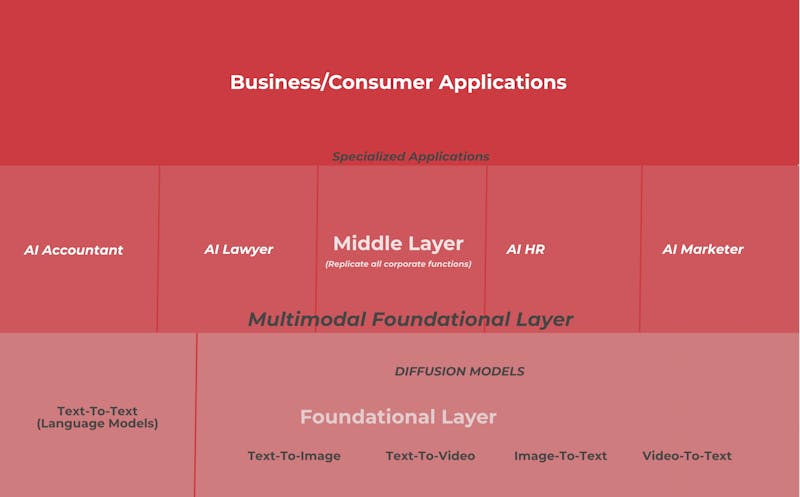

In the three layers of AI theory in the AI Business Models book, I explained in detail what the AI business ecosystem looks like.

For this analysis, I’m leaving out the other core layers (hardware and cloud infrastructures), which I’ll tackle in the second part of AI moats.

There, I explained how, on the software side, the industry is developing according to three layers:

-

Foundational Layer: General-purpose engines like GPT-3, with features such as being multi-modal, driven by natural language, and adapting in real-time.

-

Middle Layer: Comprised of specialized vertical engines replicating corporate functions and building differentiation on data moats.

-

App Layer: The rise of specialized applications built on top of the middle layer, focusing on scaling up the user base and utilizing feedback loops to create network effects.

Now, once you’ve understood that, let’s see what – I argue – can create a competitive moat in AI.

If you need more clarity, jump here and read it all!

This is part of a whole new Business Ecosystem.

In short:

-

Software: we moved from narrow and constrained to general and open-ended (the most powerful analogy at the consumer level is from search to conversational interfaces).

-

Hardware: we moved from CPUs to GPUs, powering up the current AI revolution.

-

Business/Consumer: we’re moving from a software industry that is getting 10x better as we speak by simply integrating OpenAI’s API endpoints to any existing software application.

What it means is that code is getting way cheaper, and barriers to entering the already competitive software industry are getting much, much lower.

At the consumer level, first millions, and now hundreds of millions of consumers worldwide, are getting used to a different way to consume content online, which can be summarized as the move:

From indexed/static/non-personalized content to generative/dynamic/hyper-personalized experiences.