{kind=link}

Currently, there are about 15 million individuals and businesses in collection with the Internal Revenue Service (IRS). The IRS initiates a collection action when a business or individual fails to make an attempt to pay or resolve his or her tax debt.

Every year, the IRS releases new data on delinquent collection activities. It shows returns filed with additional tax due, returns not filed in a timely way, offers in compromise, and enforcement activity.

You can download this data via a series of Excel spreadsheets on the IRS website. The data includes multi-year comparisons for the time periods 1994-2001 and 2002-2010. After that, the format of the report changed so it shows current versus prior year stats only. A multi-year comparison is not possible unless you download each of the individual annual reports and manually aggregate them into a single table.

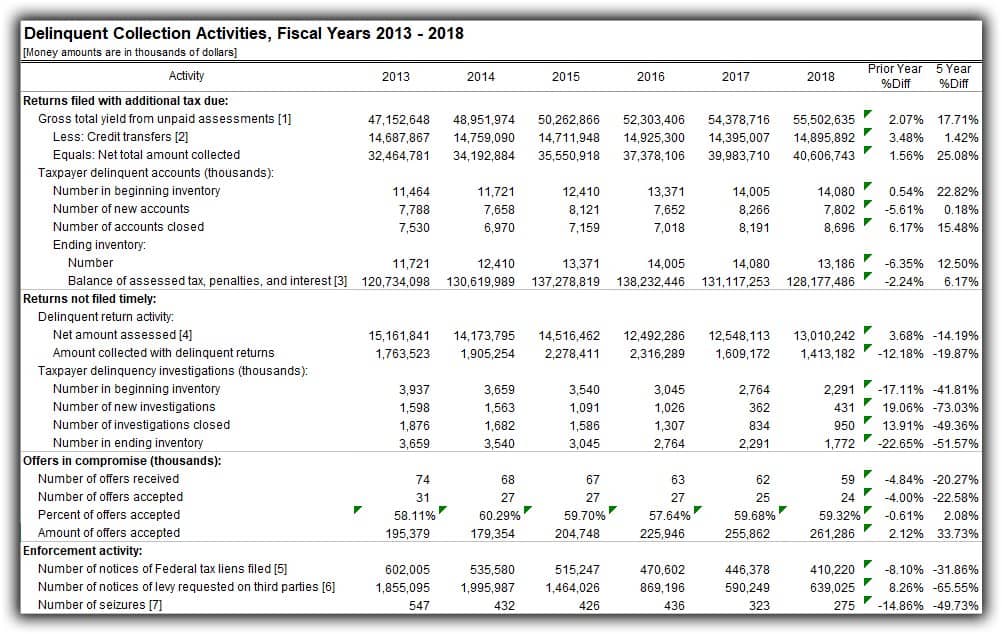

IRS Delinquent Collection Activities 2013 – 2018

That’s what we did.

The table below shows a comparison of the last 5 years of IRS delinquent collection activities – fiscal years 2013 through 2018. A little green triangle in the top left-hand corner of a cell indicates the cell value has been calculated by us, using the IRS provided data.

Terminology

A few definitions might help:

- A delinquency investigation is opened when a taxpayer does not respond to an IRS notice of a delinquent return.

- An offer in compromise is a proposal by a taxpayer to the Federal Government that would settle a tax liability for payment of less than the full amount owed. Absent special circumstances, an offer will not be accepted if the IRS believes the liability can be paid in full as a lump sum or through a payment agreement.

- A tax lien is a government claim on your property and is generally placed when a business or individual taxpayer fails to pay taxes owed. It does not mean taxation authorities will seize your property, it just ensures they get first right to your property over other creditors.

- A tax levy is the legal seizure of taxpayer assets to satisfy back taxes owed.

Highlights of the 5-year comparison are described below.

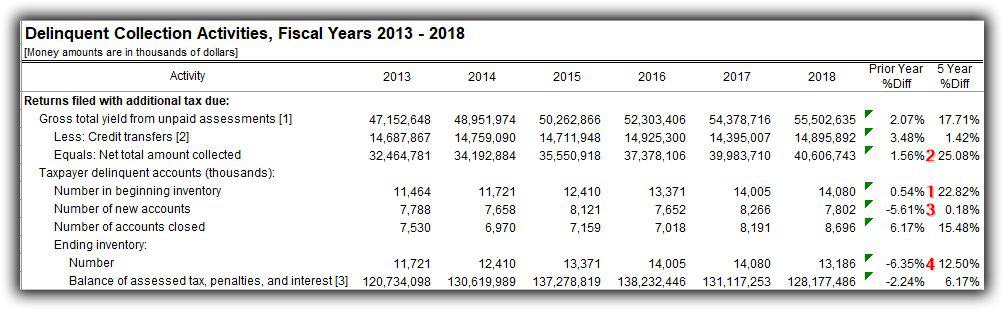

Returns Filed With Additional Tax Due

There has been a definite uptick in the number of files returned with additional tax due over the last 5 years. Not surprisingly, the amount owed to the IRS has also risen.

- The Number of Delinquent Accounts has grown 22.82% over the last 5 years, from 11,464,000 in 2013 to 14,080,000 in 2018.

- Net Total Amount Collected in 2018 has also increased significantly, to $40,606,743. This includes amounts collected through collection activity on previously unpaid assessed taxes, plus amounts assessed an accrued penalties and interest, minus credits transferred from one tax module to another where the receiving module is in collection status. It represents a 25.08% increase over 2013.

- The number of New Taxpayer Delinquent Accounts went down 5.61% in 2018 (from 8,266,000 to 7,802,000). The metric has held relatively steady over the past five years though. The 5-year difference is a mere 0.18%. The 5.61% drop in 2018 may be due to the fact that more accounts were closed last year than in previous years. 8,696,000 accounts were closed in 2018 vs 8,191,000 in 2017, a 6.17% increase.

- The Ending Inventory of Taxpayer Delinquent Accounts was 13,186,000 in 2018, up 12.50% from 2013.

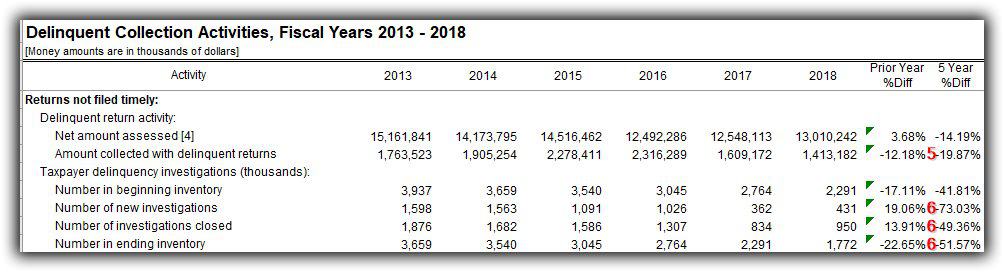

Returns Not Filed Timely

Returns not filed in a timely way and the amount collected with delinquent returns have both dropped significantly over the last 5 years, the biggest downturn having started in fiscal year 2017 (tax year 2016).

- The Amount Collected With Delinquent Returns dropped from a high of 2,316,289 in fiscal year 2016 to 1,413,182 in 2018 signaling a near 40% drop, a 19.87% drop from 2013.

- The Number of New Investigations, Investigations Closed, and Investigations in the Ending Inventory all dropped by significant amounts, by 73.03, 49.36, and 51.47% respectively.

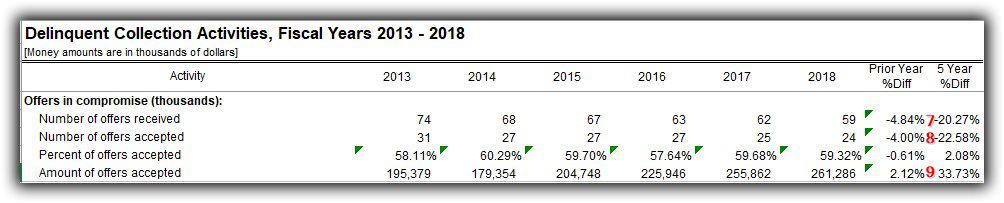

Offers In Compromise

- The number of offers in compromise received has slowed over the last 5 years, down from 74,000 in 2013 to 59,000 in 2018 – a 20.27% difference.

- The number of offers accepted has also gone down. 22.58% fewer offers were accepted in 2018 than in 2013, a quantity that closely mirrors the drop in offers received.

- The dollar amount of offers accepted has gone up significantly, by 33.73%. Year-over-year numbers show a steady climb since 2015 and then a slight down-turn in 2018.

Liens, Levies, and Seizures

While the number of returns filed with additional tax due has increased over the past five years, the number of Federal tax liens filed, levies requested on third parties, and seizures have all gone down.

- Federal tax liens filed have gone down steadily by an average of 7.30% over the last 3 years. That represents a 31.86% total drop in federal tax liens filed since 2013.

- The number of notices going out to taxpayers explaining a levy has been requested on third parties has gone down 65.55% since 2013.

- The number of seizures conducted by the Field Collection program has gone down 49.73% since 2013 with the biggest reduction (25.92%) having occurred in fiscal year 2017, tax year 2016.