Choosing the right corporation type is important for startup founders and small business owners. That decision has implications for raising capital, taxes, liability protection, and more.

The most common business entities are:

- Limited liability company (LLC)

- C corp

- S corp

- General partnership

- Sole proprietorship

This article will compare and contrast the impactful differences, so you can decide which is right for you.

12 Facts About SBA Loans That Surprise Most Business Owners

Considering an SBA loan? Here’s what you should know before you apply.

The Most Common Corporation Types in the United States

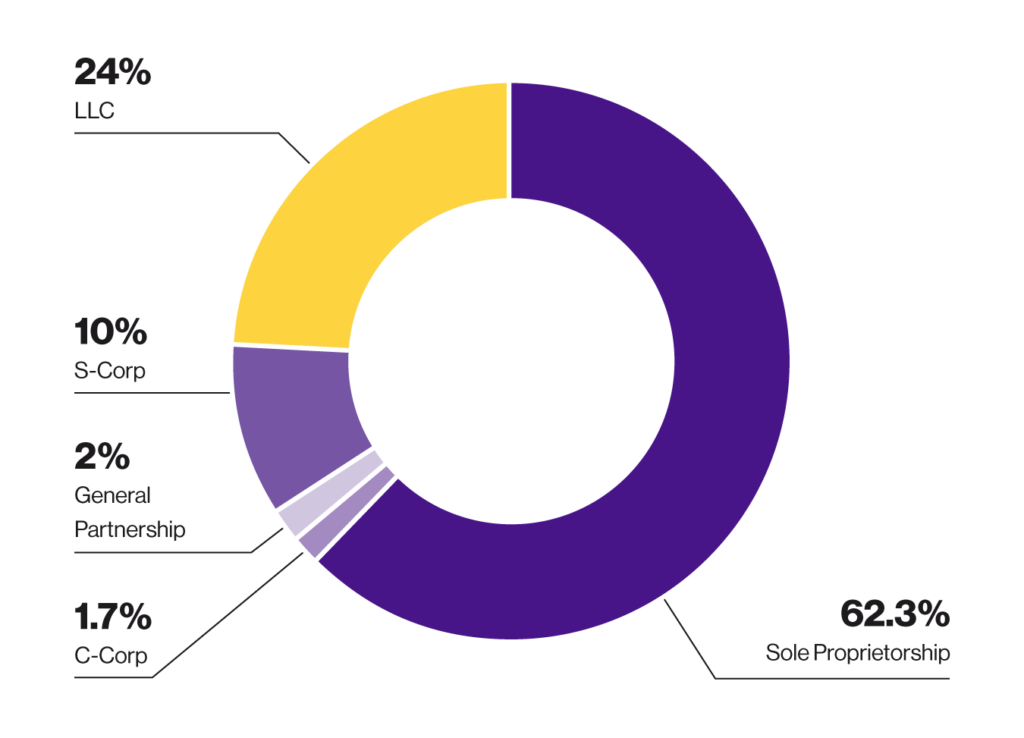

Each year, the Census Bureau collects all manner of data. Their most recent survey found that of the nearly ~35 million businesses in the US, organizational structures broke down as follows:

Let’s look at each in turn.

Sole Proprietorship

A sole proprietorship isn’t technically a corporation; it’s a business run by a single person who hasn’t registered to operate under a separate legal entity. Unless you actively choose otherwise, business owners are automatically considered sole proprietors.

Under this structure, there is no separation between you and the business. Profits and losses “pass through” to the individual level, where you’ll pay both personal income and self-employment taxes. Additionally, you’re personally responsible if the company gets sued, and all business debts are your debts.

This is reasonable if you want to test an idea. However, once you’ve committed, creating a legal entity to run the business through is best. Banks are more likely to loan you money, investors take you more seriously, and you can more easily establish credibility with customers.

Limited Liability Company (LLC)

An LLC creates a legal distinction between yourself and the business. If the company goes bankrupt, or faces a lawsuit, your personal assets won’t be at risk. Like sole proprietorships, business revenues and expenses flow through to regular income and self-employment taxes.

Registering an LLC is relatively simple: choose a state, choose a name, and file your articles of incorporation. Afterward, apply for an employer identification number from the IRS, which you’ll use to open a business bank account. Depending on where you incorporate, there will be a small fee as well as a requirement to file annually with the state.

| Important: Business owners are often encouraged to incorporate in Delaware, but this is unlikely to benefit you unless you’re a large corporation or venture-backed startup. Read why in our article on Why Companies Incorporate in Delaware. |

General Partnership (GP)

General partnerships are sole proprietorships, except more than one person owns and operates the business. Unless you take a specific action, you and your partners are considered general partners by default.

Doing business this way offers no personal asset liability protection. Additionally, profits and losses pass through to regular income taxes.

Partnerships can also be organized as limited partnerships (LP) and limited liability partnerships (LLPs). Under an LP, one partner has unlimited liability while all others have personal asset protection. Under an LLP, all partners have limited liability protection. You must formally register in order to organize as an LP or LLP.

C Corporation (C Corp)

These are also legal entities distinct from their owners. Like an LLC, shareholder personal assets are not at risk if something happens to the company. However, this company type is different from LLCs in various ways, but two in particular: they’re designed to issue ownership shares, and they face double taxation.

When the company makes a profit, it’s responsible for paying corporate income tax. From here, if it chooses to distribute remaining profits to shareholders, they will pay income tax on those dividends.

C corps are common among publicly traded companies due to how easily they can raise capital by issuing equity. Of course, LLCs can also have shared ownership, but C Corps are better for large numbers of shareholders.

In addition, C corps are responsible for holding at least one shareholder meeting per year, have special record-keeping and reporting requirements, and are subject to a higher level of regulatory scrutiny than other business structures.

S Corporation (S Corp)

S corps are similar to C corps, but treated differently by the IRS. While a C corp is subject to corporate taxes, an S corp is a pass through entity that taxes shareholders only at the individual level.

If they could, most C corps would probably opt to be treated as S corps. However, because this entity cannot have more than 100 shareholders, they aren’t a good fit for companies with large numbers of shareholders. See here for a comprehensive list of S corp eligibility requirements.

LLCs can elect to be treated as S corps.

LLCs can elect to be treated as S corps. This decision has some complicated tax consequences, but in some cases, saves owners money on self-employment taxes. It’s wise to consult with a tax professional before making this decision.

Comparing Common Business Structures

Choosing your business entity is no easy task. Let’s do a quick comparison of the significant differences from type to type.

What Is the Difference Between a Sole Proprietorship and an LLC?

Both business types are pass through entities, where owners pay self-employment and individual income taxes. The primary difference is that LLCs offer personal assets protection while sole proprietorships do not.

Other differences include:

- LLCs can more easily raise funds from investors or get bank loans

- LLCs can choose to be treated as S corps, where they may save money on self-employment taxes

- LLCs have to formally register with the state

Even if you’re relatively new to business, it’s worthwhile to establish an LLC. The liability protection is valuable on its own. Plus, you can start building credit history under your business name. It will be a while before you can get a bank loan without a personal guarantee, but if you build your credit history early, this time may come sooner.

| Important: Separating business and personal expenses can be a challenge for new business owners. At minimum, having dedicated business credit cards and bank accounts is a good idea. Doing so makes tracking expenses and making informed decisions easier. Read our article on Cash Flow Management for Startups for more tips and best practices. |

General Partnership vs LLC

Since a general partnership is simply a sole proprietorship with multiple partners, the same differences as the above section apply.

LLCs offer personal liability protection, while general partnerships do not. You’ll also have to register with the state to form an LLC and find obtaining a bank loan under a general partnership is more challenging.

LLC vs S Corp

Both entities offer pass through taxation and limited liability protection to their owners. However, S corps offer two distinct advantages over LLCs:

- It’s easier to raise capital by issuing ownership shares

- S corps can sometimes save money on self-employment taxes

LLCs can sell equity in the company by bringing on new partners. However, S corps are better for startups seeking venture capital since they can issue stock.

S corps can compensate owners via salary and/or dividend payments. Since salaries are subject to self-employment taxes, while dividends are not, there’s potential to minimize self-employment tax by optimizing payment structures. Keep in mind that it’s not legal to pay yourself no salary at all; the IRS requires your compensation to be within a reasonable threshold of what a regular employee would make in your industry.

S corps also have drawbacks to consider. They’re more expensive to register, cannot include non-US citizens as owners, and must adhere to corporate governance practices to maintain their status.

| Type | Ownership | Liability | Taxes | Fundraising |

| Sole proprietorship | One person | Unlimited | Personal income Self-employment |

Personal credit |

| General partnership | Two or more | Unlimited | Personal income Self-employment |

Personal credit |

| Limited Liability Company (LLC) | At least one | Personal assets protected | Personal income Self-employment |

Personal credit Business credit |

| S corp | At least one, maximum 100 | Personal assets protected | Personal income Self-employment |

Personal credit Business credit Stock |

| C corp | Unlimited | Personal assets protected | Corporate income Personal income |

Personal credit Business credit Stock |

Conclusion

Sole proprietorships and general partnerships are the most straightforward business entities. Unless you register otherwise, you’re automatically opted in. LLCs are the next most common, offering personal asset protection by separating yourself from the business. C corps are complex organizational structures which are beneficial to companies interested in selling stock or going public. Finally, S corps are a special type of LLC that, for qualifying companies, comes with potential tax benefits and the option to sell stock.

Are you a startup founder wondering how to organize your business? Contact an indinero financial expert for a complimentary consultation. We’ve worked with hundreds of companies over the years and can confidently guide you in the right direction.