{kind=link}

When you’re building a tech startup, accounting probably doesn’t feel very exciting. Who wants to think about spreadsheets when you’re busy building or scaling?

But, as a Y Combinator funded company and referral partner, we’ve noticed a pattern: promising startups regularly fail because of poor financial management.

In this article, we’ll explore the essentials of tech startup accounting, including best practices, common mistakes, and the accounting software we think will make your life easier.

Is Your Business Financially Ready to Raise Funding?

Download your Series A checklist:

The Importance of Accounting for Tech Startups

Accounting is about more than compliance. Startups that hope to attract venture capital need to be able to provide high-level financial statements to investors. Not only does it speed up their due diligence, but founders who practice good financial hygiene are better equipped to make informed decisions, manage cash flow, and demonstrate the discipline that builds confidence among investors.

Good accounting also helps avoid costly mistakes: misfiled taxes, underreported equity, or mismanaged cash flow can snowball into major problems.

|

Important: Startup funding deals fall apart all the time because of this oversight. Don’t make this mistake.

Presumably, the value of shares will increase over time. Without an 83(b) election, the IRS will treat that increase as taxable income. As a result, founders who don’t make 83(b) elections are less attractive to investors or collaborators.

|

What’s Unique About Tech Startup Accounting?

Conventional companies and startups are different enough, but tech startups come with an added layer of complexity that’s important to consider. Let’s explore what makes tech startup accounting unique.

Revenue Recognition Timing: Cash vs. Accrual

This is one of the more common reasons startups come to us for help. If you run a SaaS business model, revenue recognition is trickier than just recording money when it lands in your account. Since customers often pay upfront for long-term subscriptions, you need to defer revenue across the length of the service.

The key is the difference between cash and accrual accounting.

You’re already familiar with cash accounting; it’s how people manage household budgets, where transactions count when money physically changes hands. Accrual accounting is a bit trickier. This method recognizes revenue and expenses at the time the service is provided, irrespective of when money changes hands.

Accrual accounting is better suited for tech startups. It requires more sophisticated accounting but is more accurate and, if applied strategically, can even save a company money on taxes.

How to Value Intellectual Property?

Intellectual property is often the crown jewel of a tech startup. Whether it’s software, a proprietary algorithm, or a patent, your IP might be a key driver of investor valuation. But accounting for IP isn’t as simple as listing it as an asset.

There are multiple valuation methods to consider, and you’ll need to decide whether the costs associated with development should be capitalized (spread over time) or expensed immediately. Each approach has tradeoffs, but regardless, there are also regulatory requirements to be wary of when listing IP as an asset.

Equity

Equity is one of the most significant sources of accounting complexity for tech startups. Tracking cap tables, understanding stock options, convertible notes, SAFE agreements, and compliance with tax laws isn’t easy. When it’s time to allocate equity, be sure to get help from an expert.

Y Combinator CFO Kirsty Nathoo, in a lecture at Stanford, shared the following advice to aspiring founders wondering about how to navigate equity allocation:

- If equity allocation among founders is very disproportionate, that’s a red flag. In YC companies with the highest valuations, there are zero instances where the founders have a significantly disproportionate equity split.

- Founders often give considerable credit, and equity, to the person who had the idea for the company. But execution is far more valuable. The effort and teamwork it takes to execute a vision is what drives success.

- The standard vesting period in Silicon Valley is four years with a one year cliff.

- Equity for founders should be subject to vesting schedules. People need skin in the game to incentivize them to continue working. It’s also a valuable way to build culture and set an example for employees.

- Even if you’re a founder, creating and signing a stock purchase agreement is important. Just as an employee receiving stock as compensation would expect to sign a document, you should too.

Unique Cost Structures

Unlike traditional businesses, tech startups spend heavily on R&D, software development, and IT infrastructure. Many of these costs can be deducted or depreciated, which can reduce tax liability, but doing so requires careful accounting and reporting.

Rapid Growth and Scaling

If all goes well, your startup could go from a small team to a global operation in just a few short years. That kind of change brings unique accounting challenges, from managing increased transaction volumes to navigating multi-state and international tax rules.

For instance, if you expand internationally, you may have to navigate “transfer pricing” laws, which govern how revenue is allocated and taxed among business entities you own across different countries. Without proper expertise, this complexity could quickly become overwhelming.

Accounting Metrics Every Startup Should Monitor

There are an overwhelming number of variables you could keep track of. It’s easy to lose the forest for the trees. But when you’re short on time, there are a handful of variables you should always monitor regularly:

Money In (Accounts Receivable): What revenue is coming in, and when.

Money Out (Accounts Payable): What expenses are due, and when.

Burn Rate: How much more you’re spending than earning.

Bank Balance: How much cash and other liquid assets are available.

Runway: How long before cash runs out; calculated by dividing bank balance by burn rate. Conventional wisdom suggests maintaining at least six savings in the bank.

While these five metrics won’t replace a comprehensive financial strategy, they will help you focus on what matters most: keeping track of cash flow and ensuring you remain financially stable.

For more information, we cover detailed KPIs in our financial planning for SaaS startups article.

| Pro tip: Watch out for “lumpy” expenses. Legal fees, office deposits, and other large one-time purchases can distort your burn rate and runway calculations. To avoid getting off track, budget for both conservative and optimistic scenarios. |

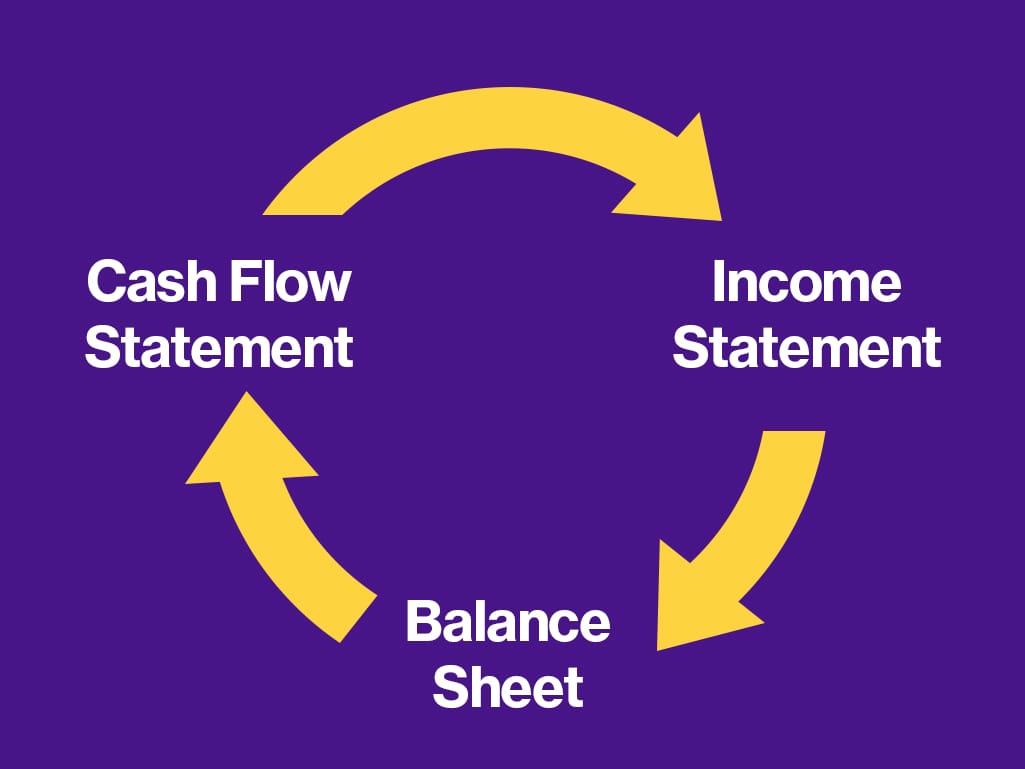

The Three-Statement Financial Model

As a founder, you understand your business inside and out. You’ll know your runway, your business model, and the likely impact different tweaks or investments might have on your business. But when it comes time to communicate your vision to stakeholders or pitch investors, you’ll need these three fundamental financial statements.

One of the first things indinero does with early-stage companies is provide fundraising support with a three-statement [cash flow, income, balance sheet] financial model. The goal is to understand the drivers of a business so that we can help with investor relations, board decks, presentations, and liaise with banks or institutional investors.” – Brian Johnson, indinero fractional CFO

Cash Flow Statement

This statement looks at a company’s ability to meet short-term obligations by tracking cash coming in and out over time. It’s divided into three sections:

- Operational: Funds from core business activities.

- Investing: Long-term asset purchases that will pay off over the long term.

- Financing: Capital earned by selling equity or soliciting loans from lenders.

The trick to understanding a cash flow statement is that only money that changes hands is counted. Invoices that haven’t been paid, loans that haven’t been dispersed, and equity deals that haven’t been closed aren’t reflected here.

For a deeper dive, read our article on cash flow management for startups.

Income Statement:

Also called the profit and loss (P&L) statement, this report summarizes revenue, expenses, and net profit over time. At first glance, it probably sounds similar to the cash flow statement, but differs in important ways.

The purpose of the income statement is to measure profitability, while the cash flow statement is only interested in whether a company can meet short-term expenses. For comparison, one statement treats loans as an influx of cash, while the other records interest as an expense against profitability. Additionally, income statements operate on an accrual basis, while the cash flow statement only registers flows only when money changes hands.

Balance Sheet

Balance sheets provide a snapshot of a company’s financial position at a specific point in time. It lists a company’s assets (what it owns), liabilities (what it owes) and equity. The fundamental balance sheet equation is:

Equity = Assets – Liabilities

Accounting vs Bookkeeping

Most tech startup founders have backgrounds in coding rather than finance, so if you’re new to this world, you might wonder about the difference between an accountant and a bookkeeper.

In short, bookkeepers are record keepers. They handle day-to-day transactions such as accounts receivable and accounts payable. Their work keeps the house in order and serves as the basis of accounting.

Accountants operate on a higher level. They prepare financial statements, handle tax filing, and help businesses strategize for the future. They’re well-versed in GAAP (Generally Accepted Accounting Principles), help navigate differences between cash and accrual accounting, and help startups design equity structures.

All startups need a bookkeeper; that could be a DIY founder or something you outsource. Whether you need an accountant depends on your growth stage, but at the very least, consider hiring help for end-of-year taxes. There are more critical things for founders to do than IRS compliance.

Accounting Best Practices

Accounting isn’t the most glamorous part of running a business, but following some best practices will save you time, money, and headaches down the road.

- Keep personal and business bank accounts separate.

This is an easy mistake to make when you’re getting started, but crucial to avoid. Mixing expenses creates confusion, eliminates the personal liability protection an LLC provides, and makes fundraising considerably more difficult. - Check your financials on a regular basis.

You’d be surprised how many founders don’t do this regularly. Regular reviews give you the insight to make informed decisions, catch problems early, and keep goals on track. - Look for negative numbers in your projections and unusual variances in expenses.

These issues can raise red flags, but more often than not, they’re just simple data entry errors. It’s easy to accidentally record an expense twice, especially if you’re doing DIY bookkeeping. - Use dedicated bank accounts and credit cards for expense and activity categories.

Using separate accounts for different tasks – such as payroll, marketing, or operations – makes managing budgets easier. When accounts are deliberately organized, it’s easy to catch a spiking expense or dipping revenue source. - Provide invoicing protocols to suppliers, contractors, and clients.

Guidelines on when and how to submit invoices, what details to include, and expected timelines for payment help avoid disputes and ensure everyone is paid promptly. The reduced back-and-forth streamlines your accounts payable and receivable processes and strengthens relationships with key partners. - Create process documents for training.

As your startup grows, you’ll delegate many tasks you’ve been accustomed to doing yourself. Documenting the processes you’ve developed makes it easier to onboard new team members while ensuring accuracy and consistency. Plus, having a written record minimizes the risk of knowledge gaps if you or someone else leaves the team.

Do Startups Need Accountants?

The short answer is: It depends on the stage of your startup and your specific needs.

All startups should handle their finances responsibly, especially if they’re spending investor dollars rather than their own, but the decision to hire help comes down to complexity and how you want to spend your time.

Tax returns aren’t worth a founder’s time. They have to be filed annually, so even in the first year of a company’s life, some service will need to be engaged. There are options available, such as indinero, which try to make things as effortless as possible from the founder’s point of view.” – Y Combinator CFO, Kirsty Nathoo

When Startups Don’t Need Help

In the very early days, you can manage without professional accounting or bookkeeping help. When finances are simple, it’s simple enough to review money coming in and out of your bank account and make do with DIY solutions such as Quickbooks.

However, it’s crucial to maintain copies of both digital and paper receipts. At some point, you’ll file taxes or hire help and need those records to categorize business expenses.

When Startups Do Need Help

Annual tax filing is a reason to get accounting help, regardless of what stage your startup is in. Hiring year-round support starts making sense as you grow and complexity increases. Adding employees, managing complex equity distributions, or raising money from investors are all worthwhile reasons to hire a CPA or CFO.

Bookkeeping Checklist

Well-kept books are the foundation of an accountant’s work; the better your records, the easier the accounting.

As your startup grows, you’ll expand to using multiple bank accounts, credit cards, and payment processors. These entities will keep lists of financial transactions, but you can’t rely on them as you would a bookkeeper. Begin by consolidating this information into a single internal spreadsheet or accounting software tool.

Next, you’ll need to make several key decisions and establish regular processes for maintaining the books. Here’s a brief checklist:

- Choose an accounting method: cash or accrual.

- Integrate software with your financial accounts for easy record-keeping.

- Establish an expense policy that dictates who is authorized and responsible for various expenses.

- Regularly review bank account and credit transactions for discrepancies.

- Update accounts receivable, noting payments and following up on overdue invoices.

- Double-check accounts payable, log expenses, and ensure you have enough cash to cover planned expenses.

- Categorize expenses for easier tracking, reporting, and year-end tax prep.

- Monitor burn rate and runway based on recent expenses and bank balances.

Software Recommendations

Indinero has spent years providing accounting and bookkeeping services to businesses small and large. Over time, we’ve identified some of the best off-the-shelf software on the market. Here’s a breakdown of some of the most popular options.

| Software | Known For | Ideal For |

| Bill.com | Automating accounts payable and accounts receivable workflows | Startups managing a high volume of invoices |

| Expensify | Tracking and reporting employee expenses | Teams with frequent travel or reimbursement needs |

| Receipt Bank (Dext) | Organizing and managing receipts and invoices | Streamlining document management |

| Fathom | Financial analysis and forecasting | Investor presentations and strategic management |

| NetSuite | Enterprise-level financial management | Scaling startups or global operations |

| Stripe | Online payment processing and subscriptions | SaaS, e-commerce, and tech startups |

| Gusto | Payroll, HR, and benefits management | Startups building or managing a workforce |

Common Mistakes

When you’re launching a startup, it’s easy to get caught up in building a product or finding your first customers. Accounting might naturally take a backseat. However, overlooking finances can lead to costly mistakes.

One of the most common mistakes is failing to track expenses and keep receipts. It’s easy to lose track of small purchases, but those small oversights add up, especially when it’s time to file taxes or share how you’ve been spending investor money. Consider proactively implementing Expensify or Dext to avoid this problem.

Failing to file an 83(b) election is another mistake that can have significant long-term consequences, and there’s a reason Y Combinator startup advisors harp on this with their new founders. As shares vest and increase in value, so do the income tax consequences of receiving them as compensation. By filing the 83(b) election, you can lock in the lower equity valuation for tax purposes, saving you and would-be investors considerably.

Tax compliance and deadlines also trip up some founders. Filing taxes late or misclassifying expenses can carry penalties or even trigger audits. For startups expanding into multiple states or countries, it’s easy to unintentionally run afoul of local tax laws. This is a case where knowledgeable CPAs are worth consulting with.

Some startups choose cash accounting when accrual accounting is a better fit. Cash may be simpler, but it doesn’t account for revenue or expenses as accurately as accounting. Plus, accrual accounting can lower tax burdens via strategically timed investments.

Finally, a mistake many founders regret is waiting too long to seek professional help. DIY accounting and bookkeeping can work in the earliest stages, but as financial management becomes more complex, the opportunity cost of focusing on something that isn’t your area of expertise can outweigh the money saved by avoiding outsourcing.

Conclusion

From ensuring compliance, managing cash flow, preparing for funding rounds, and scaling operations, solid accounting is important to your startup’s success.

Indinero has simplified accounting, bookkeeping, and financial management for startups of all sizes. Whether you’re starting out or preparing to raise your next funding round, we’re here to help take control of your finances. Reach out for a complimentary consultation today.