By Karl Sinclair

Boeing first quarter 2025 earnings report.

April 23, 2025, © Leeham News: As aircraft destined for delivery for airlines in China were turned around and returned to the US, the Boeing Company (BA) released 1Q2025 results today. Results were better than expected, with the loss lower than forecast and Free Cash Flow better than analysts forecast.

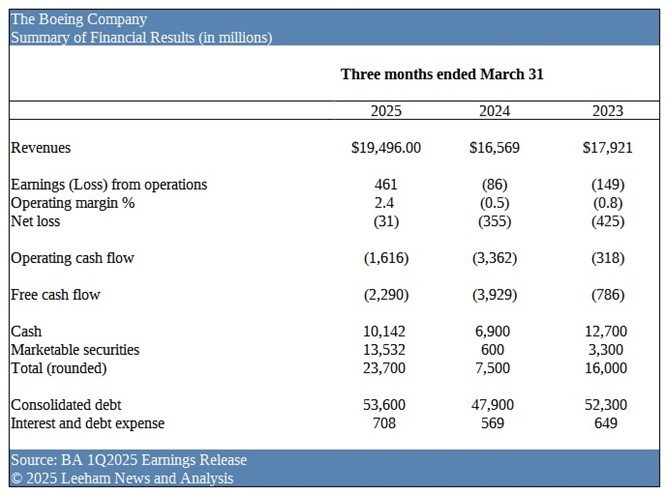

Revenue in the quarter was $19.5bn, the loss per share before charges was 49 cents and free cash flow, while negative at $2.3bn, was well below analyst projections.

Boeing ended the quarter with $23.7bn in cash and marketable securities, down from $26.3bn on Dec. 31. Debt was $53.6bn, down slightly from the end of last year. Boeing has an untapped $10bn line of credit.

The company said it still expects to return to a new production rate on the 737 MAX line of 38/mo. Production for the 787, how at 5/mo, is forecast to go to 7/mo this year. Both figures are lower than previously targeted (42/mo and 10/mo, respectively).

Yesterday, Boeing announced that it had reached a deal with Thoma Bravo – a software investment firm, to spin-off parts of the company for $10.55bn in cash. The deal includes Jeppesen, ForeFlight, AerData and OzRunways assets, and is expected to close by the end of 2025.

Planes returned from China

Two 737-8 MAX aircraft originally destined for Xiamen Airlines departed the Boeing Completion and Delivery Centre in Zhoushan, China, bound for Seattle (WA), since April 18.

While the fallout from the tariff war between the Trump Administration and the world (with an emphasis on China) have yet to fully take hold, the effects can be felt across the industry and especially in the Pacific Northwest.

The latest indications are that Donald Trump is beginning to realize the futility of tariffs and is beginning to make noises about walking them back. “They won’t be 145%, but they won’t be 0%”, he said late Tuesday, when referring to China.

Whether this is enough to placate China and restore deliveries that were halted country-wide, remains to be seen.

In its position at the top of the supply pyramid, with a customer base 80% outside of the US, Boeing faces enormous risk on both the sales and expense side of the equation.

Sale of Jeppesen

Boeing will retain some of the core digital capabilities after the sale of Jeppesen is completed but expects that some 3,900 employees will be affected in the transaction.

“This transaction is an important component of our strategy to focus on core businesses, supplement the balance sheet and prioritize the investment grade credit rating,” said Kelly Ortberg, Boeing president and chief executive officer.

Boeing had hinted in the FY2024 earnings call that it would be “trimming and pruning” the company, and since Jeppesen had been named as a target, this hardly comes as a surprise.

Company Level Results

Boeing was expecting a difficult first-half of 2025, which would level out as the year progressed. Free Cash Flow was projected to be negative, with a burn rate of between $4bn-$5bn for the year.

The company is expecting to take on an additional $4.3bn in debt, when the Spirit Aerosystems acquisition is finalized mid-year. Shareholders will get diluted to the tune of ~$4bn in the all-stock transaction.

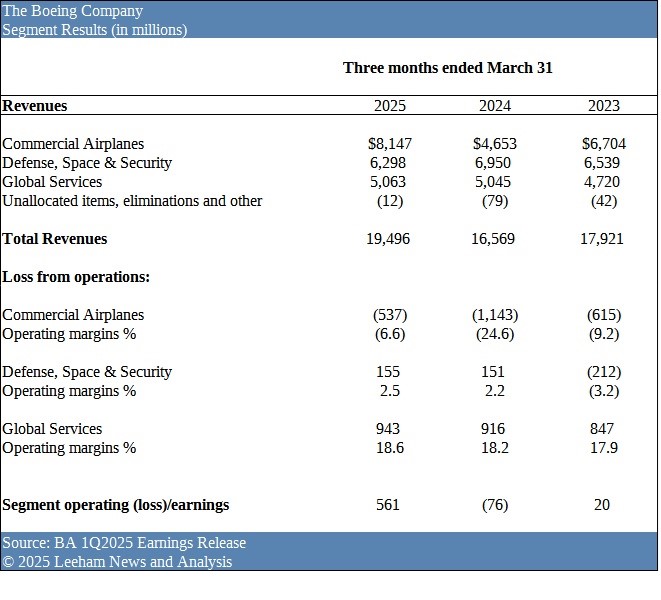

Company revenues outperformed 2023, with a 2.4% operating margin.

Company revenues outperformed 2023, with a 2.4% operating margin.

As expected, cash burn from operations was ($1.616bn) and FCF was ($2.29bn) for the quarter.

Consolidated debt, while up YOY, was relatively flat from FY2024, at $53.6bn. Interest dipped slightly from $755m to $708, over the past quarter.

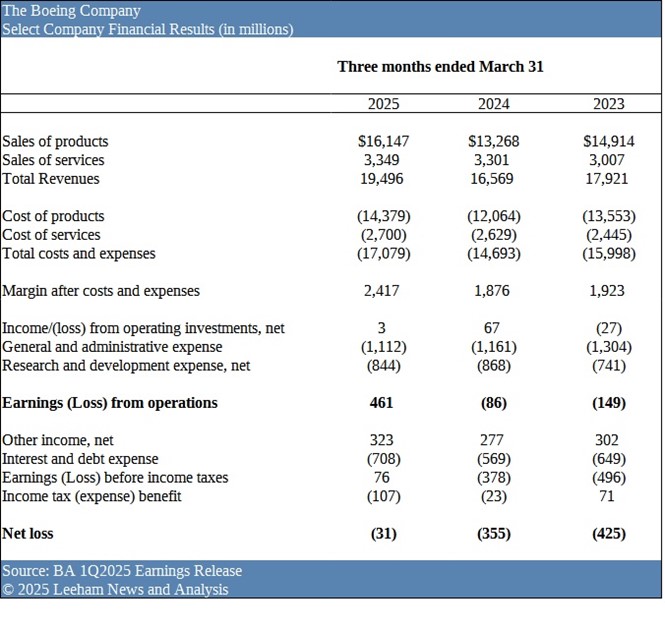

Product sales drove the increase in revenues, versus 2023 – which was the stated barometer year.

Operations produced a positive result of $461m, while the net loss narrowed to ($31m).

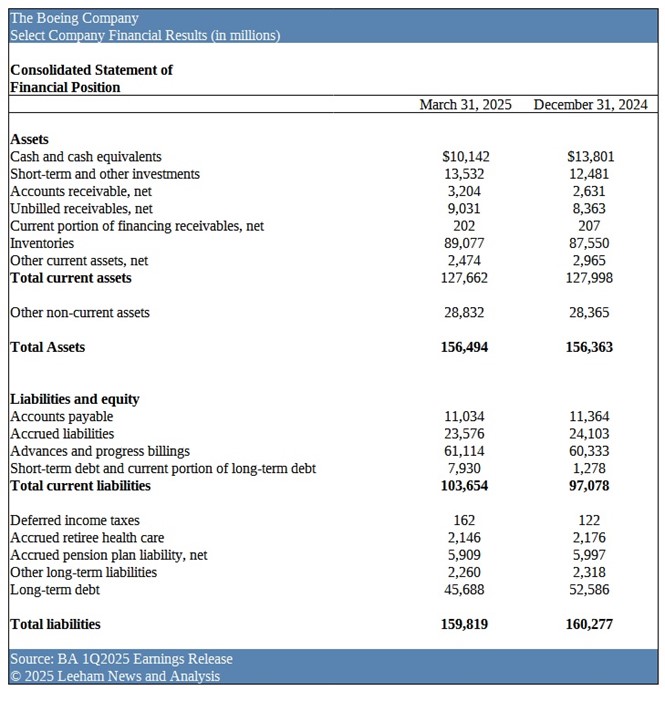

As expected, cash and equivalents dropped as the predicted cash-burn took effect in 1Q2025.

As expected, cash and equivalents dropped as the predicted cash-burn took effect in 1Q2025.

Inventories rose ~$1.5bn during the quarter, the cause of which will be determined when the 8-K is filed.

Boeing took in an added $781m in customer deposits, during the period.

Short-term debt increased dramatically, as long-term obligations become due during the year, meaning more cash spent to repay debt.

Segment Analysis

On the FY 2024 earnings call, investors were told to expect 2025 to be a repeat of 2023.

Margins at Boeing Commercial Aircraft (BCA) and Boeing Defense, Space and Security (BDS) were projected to be negative, while Boeing Global Services (BGS) was expected to continue producing profitable results.

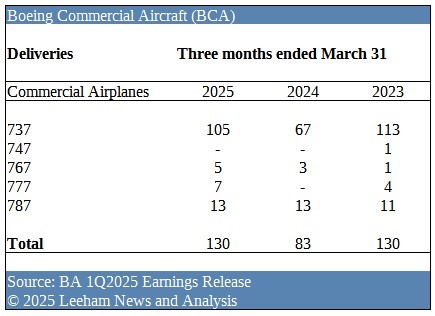

Deliveries at BCA were indeed a repeat of 2023, with an exact total of 130 aircraft turned over to customers in the quarter. Delivery mix was slanted towards widebodies with 25 delivered in 2025, versus 17 in 2023.

Deliveries at BCA were indeed a repeat of 2023, with an exact total of 130 aircraft turned over to customers in the quarter. Delivery mix was slanted towards widebodies with 25 delivered in 2025, versus 17 in 2023.

The 767 program once again showed delivery improvement, even as tanker numbers dropped, during the period.

When compared Year-Over-Year (YOY), 1Q2025 was a vast improvement, increasing dramatically from 2024 by 47 units.

This was primarily drive by pent-up inventory finally being released to customers, built up during the closing stages of 2024.

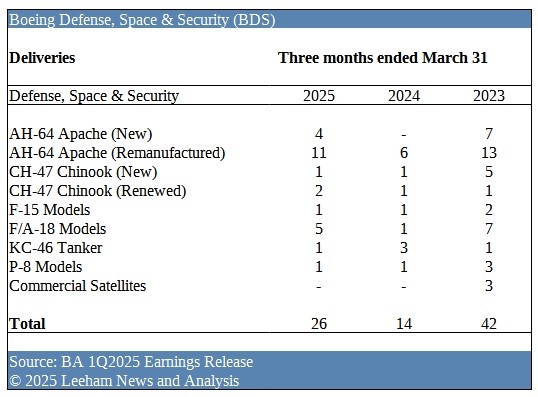

First quarter deliveries at BDS did not match 2023 levels, with only the Ch-47 Chinook (Renewed) growing modestly by a single unit increase. Every other program either declined or was relatively flat.

However, deliveries were up versus 2024, almost doubling from 14 to 26, driven by the F/A-18 and both AH-64 programs (New and Remanufactured). KC-46 Tanker numbers dropped, a result of cracks being discovered during pre-delivery inspections.

Commercial Satellites had a second consecutive first quarter with no deliveries, as Boeing tries to decide what to do with the program.

The increase in company revenues was driven by BCA, a jump of $1.443bn over 2023. This was helped by an increase in the widebody delivery mix.

The increase in company revenues was driven by BCA, a jump of $1.443bn over 2023. This was helped by an increase in the widebody delivery mix.

Margins were still negative (6.6%) but improved over previous years.

BDS earnings and margins were flat, YOY, but a welcome sign at the beleaguered division.

BGS quietly went about its business, producing a very solid 18.6% margin on sales of $5bn.

Once again

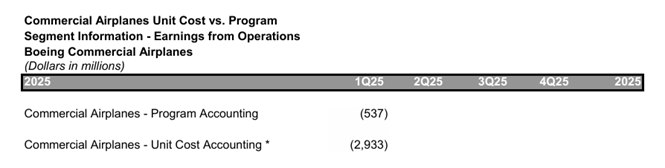

Looking deeper into the 1Q2025 results, with the help of the Boeing online unit cost vs program accounting cost page, was revealing:

BCA claimed negative margins of ($537m) during the quarter, however on a unit-cost basis, the loss was ($2.933bn), indicating that deferred production costs, stored in Inventory, will be on the rise.

~$2.4bn in costs incurred during 1Q2025 will now be capitalized, to be expensed against future deliveries.

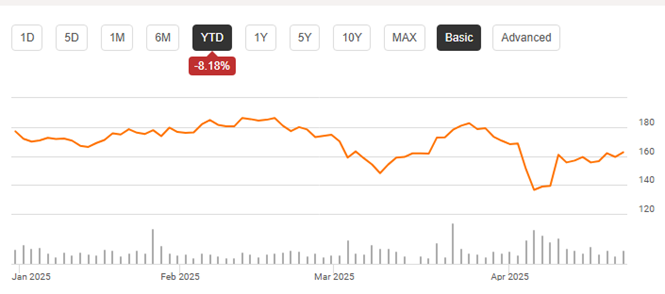

Market Effects

Boeing share price has been on a roller-coaster ride, since the beginning of the year.

Source: Seeking Alpha

Driven by the effects of the on-again, off-again, tariffs – investors have been hard pressed to judge future company performance, until a stable environment has been established.

The whip-saw swing has happened despite a slew of relatively good news, including decent delivery performance, awarding of a $20bn contract to BDS for the next-generation fighter aircraft and a bump in commercial aircraft orders.

Results will be updated following the 1Q2025 conference call with CEO Kelly Ortberg and CFO Brian West at 10:30 a.m. EST.

A further update will occur when the quarterly 8-K report has been filed with the Securities and Exchange Commission (SEC).

Related