{kind=link}

Before the article, here’s what’s happening this week on our podcast, Personal Finance for Long-Term Investors:

Reader Phil wrote in last weeK

Jesse – I appreciate everything you have to say on stock investing and low-cost, diversified index funds. I also love all the Warren Buffett wisdom you share. But, at least when it comes to investing, isn’t Buffett a counter-example to diversified indexing? How do you square that circle?

Phil

This question is like a young dad placing a baseball nicely on a tee so that little Timmy (that’s me) can step up with his $29 Wal-Mart aluminum bat and slug a double to the left-center field fence. Bam! Thanks for the setup, Phil!

Phil has a great point. The type of long-term investing I describe on The Best Interest is not how Buffett has invested over his long career. But if you follow me today, you’ll see where the common ground and divergences exist. I’ll present a “unified theory” of stock investing that connects diversified indexing and individual stock picking to the same logic.

The Core Commonality

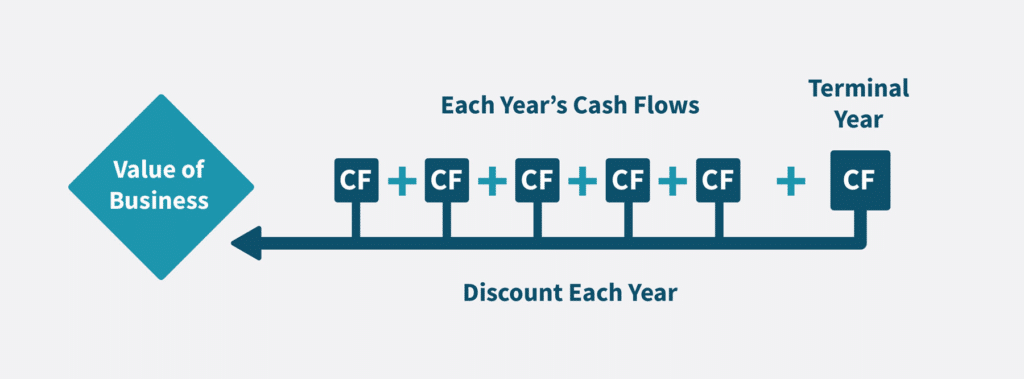

Whether picking individual stocks or buying an index fund, investors ultimately buy ownership in real businesses. Stocks are not lotto tickets. They are shares of companies, a fractional ownership of those companies’ earnings, cash flows, and assets.

Both Buffett-style investing and indexing rely on the idea that a company is worth the present value of its future cash flows. If we added up all a company’s profits “from now until Judgement Day,” as Buffett would say, “and discounted those dollars to today,” that’s the business’s intrinsic value.

But does a stock’s price always match the company’s value, as described above? That’s where some of today’s contention and confusion exist. I’d answer that question this way:

- Investors vote with their dollars. They’ll buy or sell a stock if they perceive it as under- or over-valued. On average, over time, yes, we expect a stock’s price to be correlated to the company’s value.

- But there are periods when a stock price is disjointed from its value. This is especially recognizable in retrospect.

The “efficient market hypothesis” (EMH) is the idea that all the buyers, sellers, and traders use all available information as best they can to hone in on the proper price for a given stock. It does not mean that today’s price is “correct” or “perfect,” per se. Instead, it suggests that poor schmucks like me and you can’t possibly know enough to know whether the market is right or wrong.

Put another way: “the market” has all the information about a company, while you and I only have some of that information; over time, there’s no way you and I can consistently outsmart the market or consistently beat the market’s prices.

This idea is the pillar of index investing. You can’t beat the market. Why bother trying? Just buy everything at the market’s prices, and hold for the long run.

How Buffett Invests

But this is where Buffett (and his partner Charlie Munger) disagree.

They don’t need to outsmart the market all the time. Instead, they’d argue, they need to outsmart the market sometimes. They don’t need to make smart decisions on every stock; instead, they should make very few investment choices.

Sometimes, they suggest, the market loses its mind. There’s some temporary insanity. It can be widespread or relatively narrow; perhaps most of the market is behaving efficiently, but one small corner is acting berserk. Either way, Buffett says, there are times when the market is not efficient and the market does not give appropriate prices to particular stocks.

Earlier, I wrote about “poor schmucks like me and you” not having enough info to know whether the market was right or wrong. Buffett says, “I’m different than that. I do have enough info, at times, to know whether the market is right or wrong about a particular stock.”

When Buffett identifies one of those opportunities – and the opportunity has a sufficient margin of error around it (in case his math ends up being too optimistic) – he pounces. This is the method by which Buffett has built his investing legend.

Coin-Flipping?

When faced with the idea that an investor can skillfully pick individual stocks, the hardline indexers and EMH acolytes would invoke the famous “coin-flipping metaphor.”

In fact, business school professors have done this to Warren Buffett’s face before, including in a famous 1984 debate at Columbia University, where University of Rochester *(gulp)* finance professor Michael Jensen challenged Buffett’s investing record.

“…if a large group of monkeys flipped coins and predicted if the coins would land heads or tails, over time, a small number of them would, by random chance or luck, correctly predict the outcome of a lengthy series of flips.”

Is Buffett’s record anything other than a series of lucky flips?

Buffett, in his midwestern folksy way, took the metaphor and ran with it. What if, he postulated, you follow Jensen’s monkey metaphor and get down to the best coin-flipping orangutans…only to find out they were all raised in the same zoo?!

It would beg the question: How can coin-flipping be “pure luck” if all the best coin-flipping monkeys are from the same zoo? Surely there must be something in the water or special training from the zookeeper. There must be some non-luck reason connecting all these winning orangutans.

Buffett then laid out nine individual investors who not only beat the market, but crushed the market (most for multi-decade periods) between the late 50s and the early 80s. These weren’t nine random or cherry-picked investors. Instead, all nine investors were students of Benjamin Graham and David Dodd – the two founding fathers of “value investing.” These nine investors were all “raised in the same zoo” – that is, they all followed very similar value investing philosophies.

Clearly, Buffett argues, there must be some skill in their common investing approach. This parable came to be known as “The Superinvestors of Graham and Doddsville.”

Caveats

But there are some important caveats here too.

- Buffett recognizes that many people can’t or won’t invest the way he does. So he’s on the record recommending index funds to most investors. He’s even instructed that 90% of his estate be invested in an S&P 500 index fund for his wife.

- Buffett started investing in an era with fewer computers, less instant data, and far fewer active investors looking for opportunities. In other words, the market was clearly less efficient.

- Could the nine superinvestors of Graham-and-Doddsville be an example of survivorship bias?

What About You?

But the real question for you reading at home is: Can you follow that path?

It’s not that the market is infallible. All you have to do is look at daily price movements to realize that the market is constantly wrong, though rapid to amend its previous mistakes. If it was perfect, why are the prices moving so much? How can it be off by multiple percentage points a day?

The bigger question is whether you possess the insight and information to recognize the market’s mistakes, the patience to wait for big mistakes, and the fortitude to pounce on those mistakes?

Do you want to invest this way? Most people don’t! In fact, the data is clear that even most professionals who attempt to consistently outperform the market will fail to do so. It’s hard!

Instead, most people should accept the returns of their diversified portfolio, build a financial plan around those returns, and move on.

The efficient market hypothesis is probably wrong. Or at least, it has clear flaws. But 99% of people should act as if it’s perfectly right.

Thank you for reading! If you enjoyed this article, join 8500+ subscribers who read my 2-minute weekly email, where I send you links to the smartest financial content I find online every week. You can read past newsletters before signing up.

On that note, our podcast “Personal Finance for Long-Term Investors” is by far outpacing this written blog. Tune in and check it out.

-Jesse

Want to learn more about The Best Interest’s back story? Read here.

Was this post worth sharing? Click the buttons below to share!