Before the article, here’s what’s happening this week on our podcast, Personal Finance for Long-Term Investors:

Jesse – I’m confused about how “the 4% rule” and other “safe withdrawal rates” can change so rapidly in such a short period of time.

If someone had retired in the middle of 2022 (a bear market), their “safe” withdrawal amount might be artificially low. Whereas if they had retired a mere ~6 months earlier, their safe withdrawal amount would be much higher. And this SWR is supposed to apply for life!

How can a 6-month difference in retirement date affect someone’s spending by ~20% for the next 30+ years!

I’m worried and frustrated that bad luck and bad timing might cause me to have an artificially low withdrawal rate throughout my entire retirement.

“Red” from Green Bay

First things first, great name/city combination, Red.

This is a really interesting question, and the place to start is by adding some…color.

Let’s apply a real scenario to Red’s question. We’ll look at a family who retired in July 2021. We’ll make some very simplified assumptions:

- They retired with $3M.

- They followed the 4% Rule precisely. Their initial withdrawal rate was $10,000 monthly, and they adjusted for inflation yearly.

- They’re on the young side of retirees and the FIRE movement loves stock investing anyway, so their portfolio is a little aggressive: 80% stocks, 20% bonds.

Unfortunately, this family retired right before 2022, which was a bad year for investors of all shapes and sizes.

Their portfolio remained at its initial $3M starting point for most of 2022, including a minimum value of $2.4M in October 2022. This is where Red’s question comes into focus.

[Shoutout to Zach Mullally, CFP, for creating these great charts]

If this family had to “re-evaluate” their retirement in October ’22, they’d come to two negative conclusions:

- Their $10,000-per-month withdrawals would now account for 5.0% per year ($10,000 per month = $120K per year, divided by a portfolio of $2.4M is 5%). This withdrawal rate would lead to a much higher failure rate than the 4% rule.

- Or, to maintain the conservatism of the 4% rule, they ought to reset their monthly withdrawals to $8000 per month. This is a permanent 20% throttling of their retirement lifestyle. Nobody wants that.

This scenario is Red’s nightmare, and he’s not alone. This same phenomenon occurs during every market downturn, and it is more noticeable the worse the downturn.

During the Great Financial Crisis (below), our family would have seen their $3.0M starting portfolio drop to $1.8M, a 40% decline.

- $10,000 per month would be a 6.7% withdrawal rate, or…

- To reset to the 4% rule, decrease their withdrawals to $6000 per month.

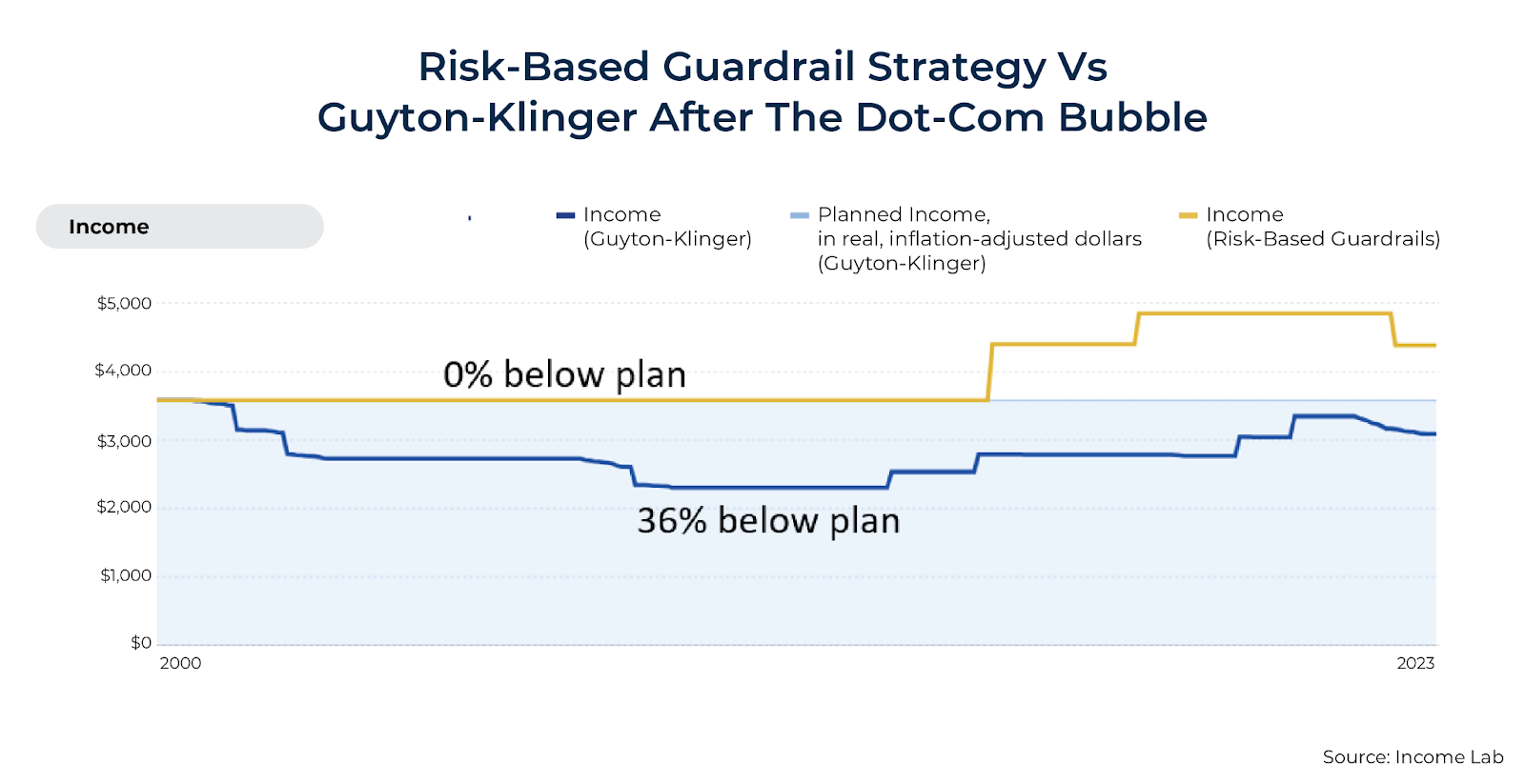

The Dot Com bubble? Same thing. A 35% decline after roughly 4 years of retirement.

What are we to do if this happens to us?!

Should we “reset” our retirement, and if so, how? Do we reduce withdrawal amounts? Pause withdrawals? Or fundamentally change our long-term financial plan? We’ll answer these questions today.

This has long been a confounding question in financial planning circles. Some experts and self-appointed nerds have attempted to create solutions, while others have pointed to simple behavioral answers. Let’s discuss some of those ideas here.

“But the 4% Rule Was Designed For This!!”

I can hear some critics now: “The 4% rule was designed for success, even when starting out in a bad market! There is no need to reset your withdrawal rate!”

This is 100% true. Here’s further reading on 4% rule basics.

But Red’s point still stands.

Technically speaking, according to safe withdrawal rate strategies (including the 4% rule), your initial withdrawal amount will set up all future withdrawals for the rest of your life.

And we’ve already established multiple real-life scenarios where a 12-month difference in retirement date could alter that initial withdrawal amount by 20%, or more.

Dynamic Withdrawal Strategies

Instead of starting with a fixed withdrawal percentage and increasing it for inflation, dynamic withdrawal strategies take a more flexible approach. They adjust withdrawals based on portfolio performance, inflation, or spending needs.

The most well-known is the Guyton-Klinger “Guardrails” strategy, which has the following “rules”:

- Start with an initial withdrawal rate (usually around 4.5%)

- Each year, increase or decrease that year’s withdrawal based on the previous year’s portfolio performance.

- If a portfolio drops and withdrawals surpass 5% per year, then decrease withdrawals by 10% to preserve capital.

- If a portfolio grows and withdrawals fall below 4%, then increase withdrawals by 10% to allow more spending.

- If the market is down, skip your inflation adjustment that year (to further preserve capital).

These “Guardrails” aren’t perfect, though. For example, a retiree following Guyton’s guardrails starting in 2000 would have spent the last 2 decades severely underspending their capability.

Vanguard has proposed a similar “guardrail” retirement system. Their recommendations are less aggressive than Guyton-Klinger’s: smaller increases during good times and smaller decreases during bad times.

However, both “guardrail” systems face the same behavioral challenge: getting retirees to comfortably, happily, and voluntarily throttle their lifestyles during bad markets.

“Buckets”

There are a few different “bucket strategies” in financial planning. This one helps us circumvent today’s “safe withdrawal rate” stress.

The idea is that we conceptually separate our retirement assets into three (or so) buckets, each with a different time horizon:

- Our short-term bucket (cash and bonds) covers 3–5 years of expenses.

- The intermediate bucket (bonds, a small amount of stocks) provides income for 5–10 years.

- And the long-term bucket (stocks, other growth assets) has the most volatility (and the most long-term growth), and replenishes the other buckets over time.

While this isn’t the mathematically perfect way to optimize a portfolio, it has fantastic behavioral and mental benefits for the investor.

How so?

Today’s “problem” is largely a function of stock performance. When stocks drag our portfolio down, our withdrawal rate can grow to uncomfortable levels.

But the bucketing method allows the investor to say “That’s a Long-Term Bucket problem, and that problem doesn’t matter for 10+ years!”

Today’s withdrawal needs are a percentage of the first bucket. And that first bucket – in theory – is highly stable. We aren’t concerned about overdrawing the first bucket. We don’t feel the same need to intentionally hamstring our desired lifestyle.

This can give investors the confidence to not tweak or disrupt their financial plan simply because stocks are in a correction or bear market. No touching!

The Bogleheads’ Variable Percentage Withdrawal (VPW)

Developed by the Bogleheads group of hardcore DIY ivnestors, the variable percentage withdrawal (VPW) method annually recalculates the withdrawal percentage annualy based on remaining life expectancy and portfolio balance.

Unlike the 4% rule, the VPW assumes no automatic inflation increases. Also, because the VPW recalculates every year as a percentage of the portfolio, the portfolio (in theory) will never run out of money.

However, that brings about a significant downside: variable withdrawals (in the name, after all!). A retiree using the VPW must be comfortable with large swings in annual spending – possibly 10%, 15%, 20% or greater swings yearly.

The “Rising Equity Glide Path”

Two major financial planning nerds – Michael Kitces and Wade Pfau – developed what they call the “rising equity glide path.” As the name implies, it attempts to smooth out retirement by increasing stock exposure over time – a counterintuitive strategy.

This strategy starts with a lower equity allocation (typically 30–40% of a portfolio) at the beginning of retirement. The primary purpose of doing so is reducing the dangerous sequence of returns risk.

Then, the portfolio slowly dials UP the stock allocation over time – roughly by 1-2% per year. This ensures sufficient growth of the portfolio throughout retirement. As the investor ages and their remaining lifespan shrinks, their “sequence risk” drops dramatically and they can afford to take on more equity risk.

All else being equal, this strategy does have greater-than-average bond allocations throughout retirement, and thus has a lower expected return. Why? Because Kitces and Pfau are willing to trade “retirement success” for “overall net worth.” I’m inclined to agree with them. It’s the age-old “bet” we’ve discussed here before. Would you rather:

- Have a 99% chance of a good retirement and dying with $500K

- Have a 50% chance of a good retirement and dying with $5M…and the other 50% is that you run out of money!

That first scenario represents a conservative plan focused on retirement success.

The second scenario represents an aggressive plan focused on maximizing growth.

Most people prefer the first. And that’s what the rising equity glide path attempts to deliver.

Back to the Original Question

Going back to Red’s original question, here’s my main takeaway:

Safe withdrawal rates and/or the 4% rule are just one of many different approaches to retirement planning. NONE of the approaches are perfect. They all have flaws, whether a lack of flexibility, a heavy burden on the individual retiree to institute drastic lifestyle changes, or an over-emphasis on caution. There is no magic bullet.

But by understanding the different approaches and viewing your retirement through various lenses, I think you’ll hone in on an appropriate approach for you. Something you can implement and stick with for many decades. My recommendation:

- Develop your financial plan – including your withdrawal strategy – ahead of time. Don’t determine your exit plan in the middle of the fire. Do it ahead of time! Consider tax efficiency,

- Back test that strategy. Give yourself historical reasons to believe this strategy will work for you.

- Specifically, understand how the “hardest” times will look for you. Will you have to throttle down your spending? Will you be comfortable withdrawing 8% from a tumbling portfolio? Etc.

- Execute and revisit. Follow your plan and periodically investigate how your plan is unfolding. While I do not recommend jumping from plan to plan to plan, I also don’t recommend going down with a sinking ship.

Thank you for reading! If you enjoyed this article, join 8500+ subscribers who read my 2-minute weekly email, where I send you links to the smartest financial content I find online every week. You can read past newsletters before signing up.

On that note, our podcast “Personal Finance for Long-Term Investors” is by far outpacing this written blog. Tune in and check it out.

-Jesse

Want to learn more about The Best Interest’s back story? Read here.

Was this post worth sharing? Click the buttons below to share!