Before the article, check out the latest on my podcast, Personal Finance for Long-Term Investors:

Now, here’s today’s article:

Today, we have a simple cautionary tale:

When it comes to retirement planning, tax planning, and other nuanced topics in the financial planning world, the devil is in the details!

I’m not trying to dunk on anybody. “The Boy Who Cried Wolf” isn’t trying to dunk on that boy. The goal, instead, is to learn a good lesson through someone else’s mistake.

Tax-Free Roth Conversions?!

One of my readers received this email from a financial firm. This firm manages between $2.5 and $3.0 billion for its clients. That’s serious money, serious business.

I read this, and for a hot second, I felt a pang of guilt over missing the boat on something so clearly beneficial for retirees. Why haven’t I heard of this yet? Shame on me! Did the OBBBA / Big Beautiful Bill create a special “tax-free Roth conversion” opportunity for retirees 65 years or older?

But then I reread it and thought:

“…these numbers are familiar. I’ve seen $6,000 and $12,000 before. And the 65-year-old threshold too…”

…and it hit me. This is NOT a new rule about Roth Conversions. Instead, this is a new general tax deduction for taxpayers age 65 and older (in addition to the existing standard deduction for seniors). Here’s the language from the IRS website:

- New deduction: Effective for 2025 through 2028, individuals who are age 65 and older may claim an additional deduction of $6,000. This new deduction is in addition to the current additional standard deduction for seniors under existing law.

- The $6,000 senior deduction is per eligible individual (i.e., $12,000 total for a married couple where both spouses qualify).

- Deduction phases out for taxpayers with modified adjusted gross income over $75,000 ($150,000 for joint filers).

- Qualifying taxpayers: To qualify for the additional deduction, a taxpayer must attain age 65 on or before the last day of the taxable year.

- Taxpayer eligibility: Deduction is available for both itemizing and non-itemizing taxpayers.

- Taxpayers must:

- include the Social Security Number of the qualifying individual(s) on the return, and

- file jointly if married, to claim the deduction.

- Taxpayers must:

There is nothing “Roth-specific” in the IRS language. This new senior deduction can and will be used to deduct any income:

- Regular work wages.

- Social Security income.

- Regular IRA withdrawals.

- Or – yes – Roth conversions.

There’s nothing specific or exclusionary about using this deduction only for Roth conversions.

My takeaway was, “That’s an interesting piece of marketing from that financial firm. But it feels incomplete. It’s somewhere in the gray middle.” I think it’s a little misleading. And this industry can’t afford to be (and shouldn’t want to be) misleading at all.

But then I went deeper.

Oh boy.

The More You Look, The Worse It Gets

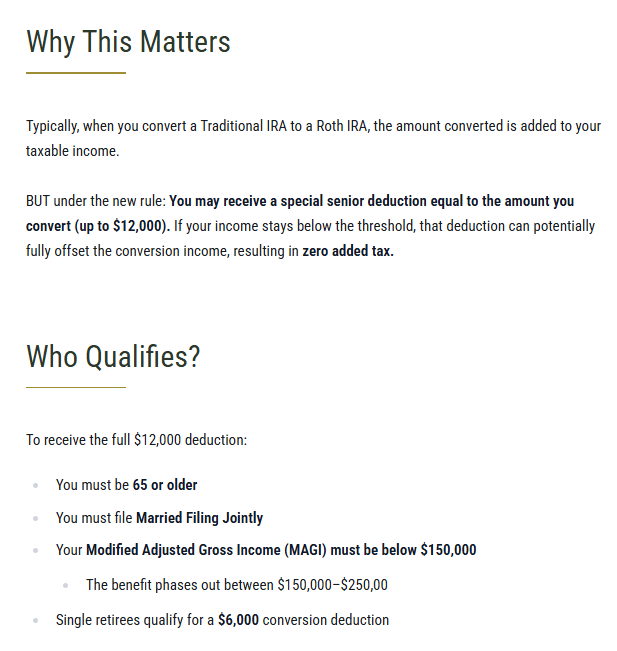

I wanted to see how this firm explained the new rules to its audience. I clicked that enticing button, Continue Here to Learn More. Here’s a screenshot from their article:

This explanation has multiple false details, namely around it being a “conversion deduction.”

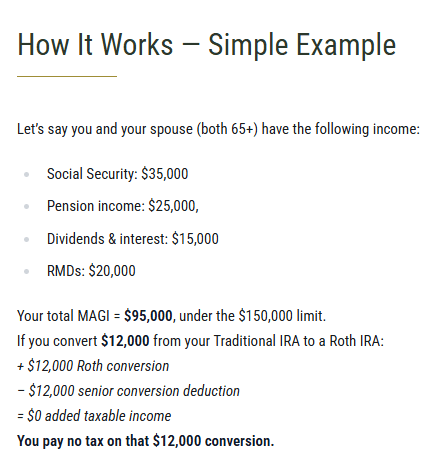

Then they provide a mathematical tax example.

“You pay no tax on that $12,000 conversion.”

Except you do.

Let’s enter these precise numbers into a 1040 tax return. What do we see?

The $12,000 conversion pushes their Taxable Income from $43,050 to $55,050. The conversion is taxed entirely at 12%, resulting in $1440 in Federal taxes.

By the time they’ve decided to convert $12,000, the new senior deduction has already been entirely consumed (all $12,000 of it) by the initial income assumptions (Social Security, pension, etc).

Yet toward the end of the example, we see them apply their so-called “senior conversion deduction” entirely to the $12,000 Roth conversion. This is plain wrong.

Proceed With Caution

Again, my intention isn’t to cry wolf, fear-monger, or dunk on another financial professional.

Instead, my takeaway is:

- This stuff can be complex.

- It has nuance.

- It deserves serious attention.

- Minor misunderstandings can compound.

This firm published their article on December 9, 2025, and is encouraging its clients to follow its directive right now in 2025, before year-end. Their clients are making incorrect Roth conversions as we speak.

None of us wants that.

The devil is in the details.

Thank you for reading! Here are three quick notes for you:

First – If you enjoyed this article, join 1000’s of subscribers who read Jesse’s free weekly email, where he send you links to the smartest financial content I find online every week. 100% free, unsubscribe anytime.

Second – Jesse’s podcast “Personal Finance for Long-Term Investors” has grown ~10x over the past couple years, now helping ~10,000 people per month. Tune in and check it out.

Last – Jesse works full-time for a fiduciary wealth management firm in Upstate NY. Jesse and his colleagues help families solve the expensive problems he writes and podcasts about. Schedule a free call with Jesse to see if you’re a good fit for his practice.

We’ll talk to you soon!