Before the article, check out the latest on my podcast, Personal Finance for Long-Term Investors:

Now, here’s today’s article:

I’m pretty good with numbers, so you can please spell out (in some detail?) an example of how tax-gain harvesting works in practice?

-MV

Let’s do it, MV. Let’s provide the nuts-and-bolts numbers behind tax-gain harvesting.

Why Tax-Gain Harvest In the First Place?

Tax-gain harvesting is the intentional act of selling an investment with a capital gain while you’re (usually) sitting in the 0% long-term capital gains bracket. Then, you immediately buy that asset back. [It’s different than loss harvesting!]

Why harvest gains?

Because done correctly in that 0% bracket, you realize the capital gain without paying any federal tax on it. That resets your cost basis to a higher level. This leads to two great long-term benefits:

- Future gains will be smaller (so future taxes shrink)

- Future rebalancing will be easier.

It’s a perfectly clean and legal “arrow” in your financial planning quiver.

Who Qualifies for Tax-Gain Harvesting?

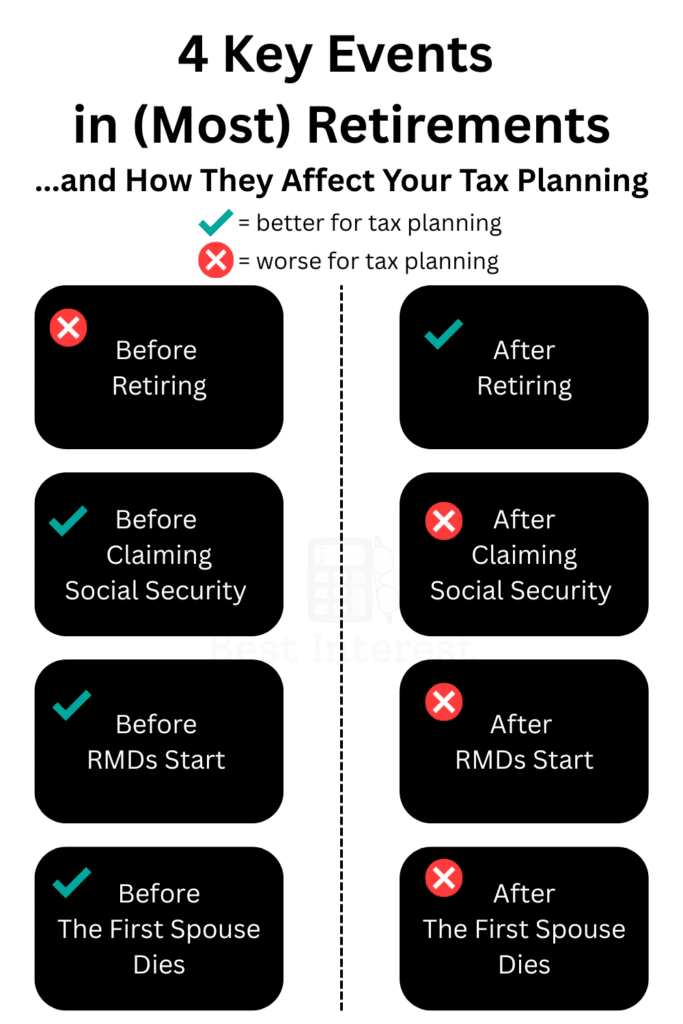

Most (but not all) retirees face a similar sequence of events in retirement that directly affects their opportunities for good tax planning (e.g tax-gain harvesting, Roth conversions, etc). The four common tax planning events that (most) retirees go through are:

- The act of retirement itself.

- Claiming Social Security

- Starting required minimum distributions

- And the death of the first spouse in a couple.

Why these events?

Because they directly impact a retiree’s tax return, via extra income and/or less space in low tax brackets.

- Retiring (usually) decreases taxable income.

- Claiming Social Security increases taxable income.

- Starting RMDs increases taxable income.

- And the first spouse dying shrinks the size of your low tax brackets.

Tax gain harvesting is most effective for people with space in their 0% long-term capital gains (LTCG) bracket.

In 2025, the 0% LTCG bracket ends at $48,350 for Single filers, and at $96,700 for Married filing Jointly. In 2026, those same brackets end at $49,450 and $98,900, respectively.

A Specific Tax Gain Harvesting Example

So let’s look at a typical retired couple somewhere in their early-60s. Going back to our “4 big events,” they’re in the following situation:

Let’s say they have $500,000 in a joint taxable brokerage account, much of which is sitting at significant capital gains. They’ve been saving and investing for many years.

They also have significant assets in both Traditional ($1.5M) and Roth ($300K) buckets.

To do effective tax planning, we need to understand their current and future tax situations. In other words, we want to know how their annual taxes will likely evolve over time. Most financial planners use nifty tax planning software to do this, but we’re going to use some rough math today.

Their Tax Situation Now

What does this couple’s tax situation look like today? It’s pretty simple.

The lower earner is collecting $21,000 per year from Social Security.

Their taxable account is spitting off about $15,000 in income and dividends. Their bank accounts, we’ll say, contribute another $2000 in interest.

…and that’s it, at least as far as “unavoidable income” is concerned.

However, it’s fair to say that many couples would need more than $38,000 in gross income to live. Let’s assume our couple needs another $62,000 per year to meet their lifestyle requirements. That’s $100K in total gross income. For the sake of simplicity, I’ll assume the $62K is all coming from Traditional IRA distributions [but (!) there is a “right” order to withdraw from your retirement accounts].

If you plug these details into a 1040 tax return, you’d find that their Federal taxable income is $65,350. This means that:

- Their marginal LTCG tax rate is 0%.

- Their marginal income tax rate is 12%.

Their Tax Situation In The Future

Though we don’t have a perfect crystal ball, we do know a few things that will occur in their future.

- The high-earner will begin collecting Social Security by age 70, which we’ll assume adds another $40,000 of Social Security income per year.

- RMDs will kick in at age 75, adding 4-5% of their Traditional IRA balance as guaranteed taxable income. It’s hard to know where their IRA balances will be in ~10 years. But it’s not unreasonable to assume they’ll be higher.

- Eventually, one of the spouses will die. The lesser Social Security income will drop away and their income tax brackets will be cut in half.

These aren’t precise guarantees, but they’re directionally accurate.

Once RMDs kick in, assume they are still filing Jointly, they’ll surely be in the 22% income and 15% LTCG brackets.

Filing Single (after the first spouse dies), they might be in the 24% income + 15% LTCG bracket.

Point being: they would rather pay taxes now (in lower brackets) than later.

They are a good candidate for tax planning.

Do You Want To Learn More?

If you’re looking for better answers to your money questions,

My free weekly newsletter helps busy professionals and retirees avoid costly mistakes and grow lasting wealth to and through retirement.

Join 4000+ subscribers, 100% free.

Sign up here:

The Actual Numbers

We’ve determined this family should pursue some thoughtful tax planning this year.

If you’re curious whether capital gains harvesting or Roth conversions make more sense…great question!

For this family, capital gains harvesting is the better option.

But how much can they “harvest?”

As a reminder, their taxable income this year is $65,350, and their 0% LTCG bracket ends at $96,700.

They can realize the difference between those two numbers – $31,350 – in long-term capital gains and pay $0 in tax on that.

That’s big.

Why Can’t They Harvest the Full $96,700?!

The most common misunderstanding in capital gains harvesting occurs when people see this table below…

…and they think, “So – as a couple, we can realize $96,700 in capital gains, and we’ll pay ZERO tax?”

That’s false. It’s important to understand how income and capital gains “stack” together.

Ordinary income takes the first space, and only afterward can capital gains stack on top. Thus, very few retirees end up getting the full “$0 to $96,700” of space to realize capital gains taxes at 0%.

Here’s a simple example, going from from left to right. We look at Ordinary Income, less Deductions, then apply Income Tax, then stack Long-Term Capital Gains on top, then apply LTCG tax rates.

The Value of Tax-Gain Harvesting

In this case, our couple harvested $31,350 in capital gains at 0% tax and reset their basis higher. Without this smart tax planning maneuver, we know that some, if not all, of that $31,350 would have eventually been taxed at 15%.

$31,350 x 15% = $4700

Rinse and repeat, year over year. It’s nothing to scoff at!

That’s a reasonable, real-world example of how tax gain harvesting works in practice.

Thank you for reading! Here are three quick notes for you:

First – If you enjoyed this article, join 1000’s of subscribers who read Jesse’s free weekly email, where he send you links to the smartest financial content I find online every week. 100% free, unsubscribe anytime.

Second – Jesse’s podcast “Personal Finance for Long-Term Investors” has grown ~10x over the past couple years, now helping ~10,000 people per month. Tune in and check it out.

Last – Jesse works full-time for a fiduciary wealth management firm in Upstate NY. Jesse and his colleagues help families solve the expensive problems he writes and podcasts about. Schedule a free call with Jesse to see if you’re a good fit for his practice.

We’ll talk to you soon!