Yes, but there is an interesting twist to the story. It is the first Fed Day of the year and the central is likely to continue cutting interest rates throughout 2025, though the exact pace is up for debate. However, something that is a bit unusual is that we currently have high interest rates, yet there is also talk about a possible bubble in US tech stocks. That’s the first time in my career that we have that combination.

If you are an experienced investor (aka ‘old’) you are fully aware that excessively loose monetary policy can fuel a stock market bubble. Most stock market excesses since the Second World War have coincided with low Fed Funds Rates relative to their recent history.

The stock market rally into the 1974 crash coincided with the Fed cutting rates aggressively from the 1969 peak. The junk bond bubble and the savings and loan crisis of 1989 were preceded by interest rates dropping from the extreme levels of the early 1980s forcing investors to stretch for yield. The tech bubble of the 1990s was helped along by the Fed keeping interest rates unchanged at relatively low levels (compared to previous experience) from 1994 onward. The financial crisis of 2008 was triggered by a housing crisis fuelled by the Fed keeping interest rates too low for too long in the 2000s.

You get the point. If the central bank keeps interest rates too low for too long, it promotes speculation and fuels bubbles in stocks and other risky assets. This is exactly what Monia Magnani found again in her analysis of the linkage between Fed Funds Rates and stock market bubbles.

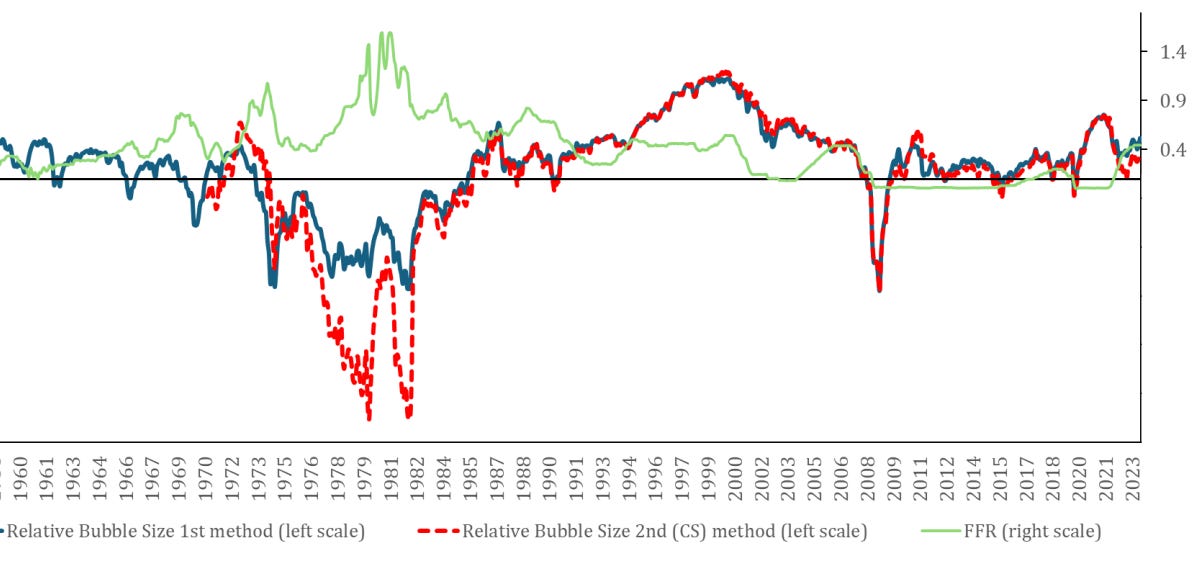

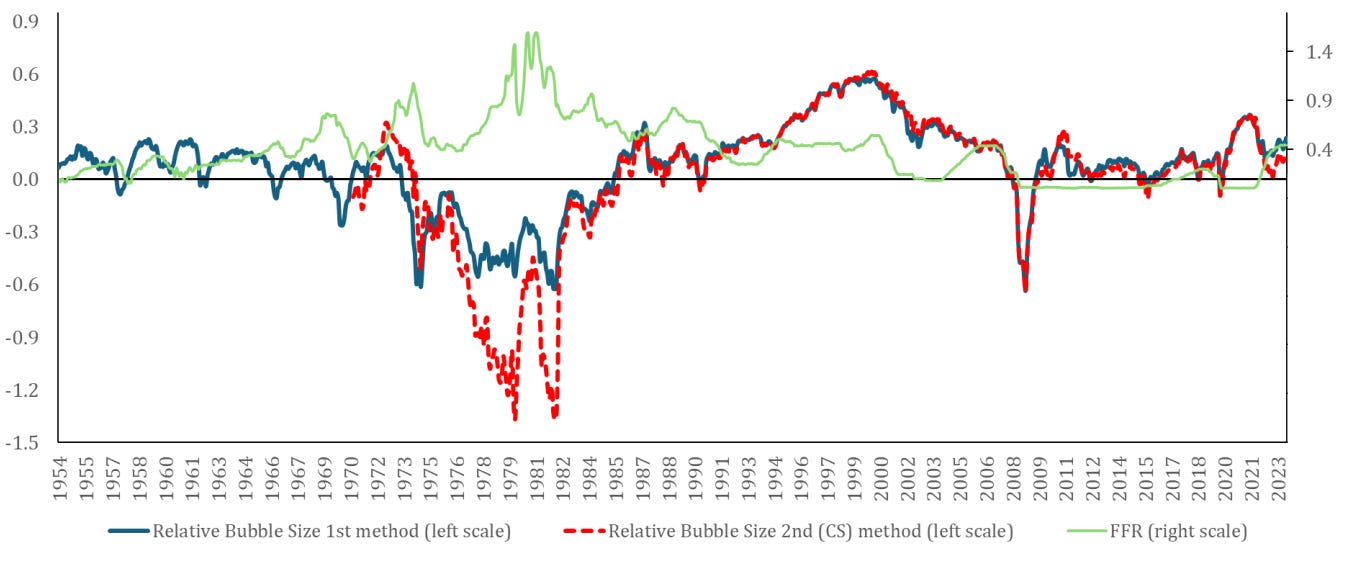

However, what caught my eye was the chart below which shows the Fed Funds Rate together with the estimated size of the bubble in US stock markets. Note that in 2020 and 2021, the rally in tech stocks during the pandemic may have created a stock market bubble that deflated with the inflation shock of 2022 and the rate hikes by the Fed.

Relative bubble size and Fed Funds Rate

Source: Magnani (2024)

But it is striking to see that stock markets were in a huge negative bubble at the end of the 1970s and in 2009. In the first instance, the Fed needed to hike interest rates to all-time highs to fight inflation and in the second the global economy nearly collapsed.

This has implications for how to assess current market valuations. If investors use low P/E-ratios as a benchmark for the ‘fair’ valuation of the US stock market, they implicitly assume that markets will drop back into a state of a large negative bubble. Investors who think that they will only invest in US stocks when the P/E-ratio drops below 10x or even 15x implicitly say that they will only invest in US stocks when they have collapsed into a negative bubble.

This is at the heart of the divergence in opinion for estimates of the equity risk premium and the true long-term fair value of stocks, as I have previously discussed. I am not making any public pronouncements of where I think the fair value for the US stock market is (for that you have to climb over the paywall of my employer and subscribe to my professional research), but the research of Magnani indicates that currently, US stock markets are not in a bubble but about 10% to 20% overvalued.