On January 27, Lockheed Martin’s (LMT) shares closed at ~$503.70. Following the release of Q4 and FY2024 results and FY2025 outlook on January 28, 2025, the share price plunged ~$46. I now view Lockheed Martin’s share price weakness as a buying opportunity and acquired an additional 50 shares @ $457.75 in one of the ‘Core’ accounts in the FFJ Portfolio on January 28. This brings my LMT exposure to 620 shares.

I last reviewed LMT in this July 24, 2024 post at which time the most currently available financial information was for Q2 and YTD2024.

When I completed my 2024 Mid Year FFJ Portfolio Review, I held 565 shares in one of the ‘Core’ accounts within the FFJ Portfolio and it was my 6th largest holding. At the time of my 2024 Year End Review, I held 570 shares and it was still my 6th largest holding. The automatic reinvestment of dividend income explains the slight increase in the number of shares.

Business Overview

LMT is a global security and aerospace company that operates in 4 business segments: Aeronautics, Missiles and Fire Control (MFC), Rotary and Mission Systems (RMS) and Space. Its main areas of focus are in defense, space, intelligence, homeland security and information technology, including cybersecurity.

It is engaged in the research, design, development, manufacture, integration and sustainment of advanced technology systems, products and services.

Principal customers are agencies of the U.S. Government. It, however, also serves international customers with products and services that have defense, civil and commercial applications.

A good way to learn about a company is to review the company’s website and Part 1 Item 1 – Business and Item 1A – Risk Factors in the FY2023 Form 10-K that is accessible through the SEC Filings section of the company’s website.

Evolving Landscape

The newly-created Department of Government Efficiency (DOGE) has some some defense stock investors on edge because of the uncertainty about what changes will be made and their impact.

A considerable amount of money, however, is wasted because of complex rules governing military planning and procurement. Current major industry participants acknowledge this. Some existing participants might welcome a more streamlined process even at the expense of more competition if changes lead to progress in speed and technology innovation.

How LMT is impacted from any changes remains to be seen. I think it is unlikely LMT’s largest program (the F-35) will experience major cuts for economic, strategic, and political reasons. Keep in mind, that this program accounts for ~26% of LMT’s sales AND it is a meaningful program for 1,900 suppliers across 48 U.S. states and 10 separate countries. We also have to consider the RTX Corp and Northrop Grumman and their suppliers also have a stake in the F-35 program.

The needs of the military organizations and the governments traditionally dictated the pace, structure, and process for technological innovations. The pace and focus, however, is increasingly being set by a progressively vocal and powerful technology startup industry and their funders and their raft of Patriotic capital initiatives such as:

The evolution of the aerospace and defense industry should be expected given the total addressable market.

Based on Verified Market Research’s 2024 – 2031 military artificial intelligence market valuation, Military Artificial Intelligence (AI) systems are expected to increase the market size from ~$13.24B in 2024 to ~$35.54B in 2031. This is because AI is increasingly being adopted to enhance decision-making, automation, and operational efficiency. If these estimates end up being accurate, we are looking at a CAGR of 14.49% during this period.

Estimates vary depending on the market data services consulted. Nevertheless, estimates are being regularly revised higher. This is not surprising considering global defense budgets have been ballooning against the backdrop of ongoing conflicts and a general shift toward militarization in the last 24 – 36 months.

The Stockholm International Peace Research Institute notes that in 2023, global defense spending reached a record level of just over $2T. The US accounted for nearly 40% of global defense spending in 2023 having spent ~$877B.

NATO’s Public Diplomacy Division report published on June 17, 2024 shows the magnitude of each member’s defense expenditure in 2014 – 2024 (the 2023 and 2024 figures are estimates).

Historically, Silicon Valley (SV) had shunned defense technology for fear of being associated with controversial overseas conflicts. In addition, SV has been wary of the Pentagon’s notoriously slow and risk-averse procurement process, which favors established defense contractors. It is not surprising, therefore, that venture capitalist (VC) funding has been directed primarily toward SV products for the civilian market.

With the war in Ukraine and geopolitical tensions with China, however, investment in military tech start-ups is booming. With the impressive growth opportunities in the defense market, VCs with large amounts of capital are increasingly directing their energy toward this market. From 2019 to 2022, US VC funding for military technology startups has doubled, and since 2021, the defense technology sector has seen an injection of $130B in VC money.

Bookings’ March 26, 2024 The evolution of artificial intelligence (AI) spending by the U.S. government research report, estimates that defense contracts for AI-related technologies grew in value by nearly 1,200% in from August 2022 to August 2023.

With the US government awarding an increasing number of lucrative contracts to Silicon Valley companies that make cutting-edge defense systems, we need to monitor the evolution of the military and defense industry.

Financials

Q4 and FY2024 Results

Refer to the material available in the Quarterly Results section of LMT’s website.

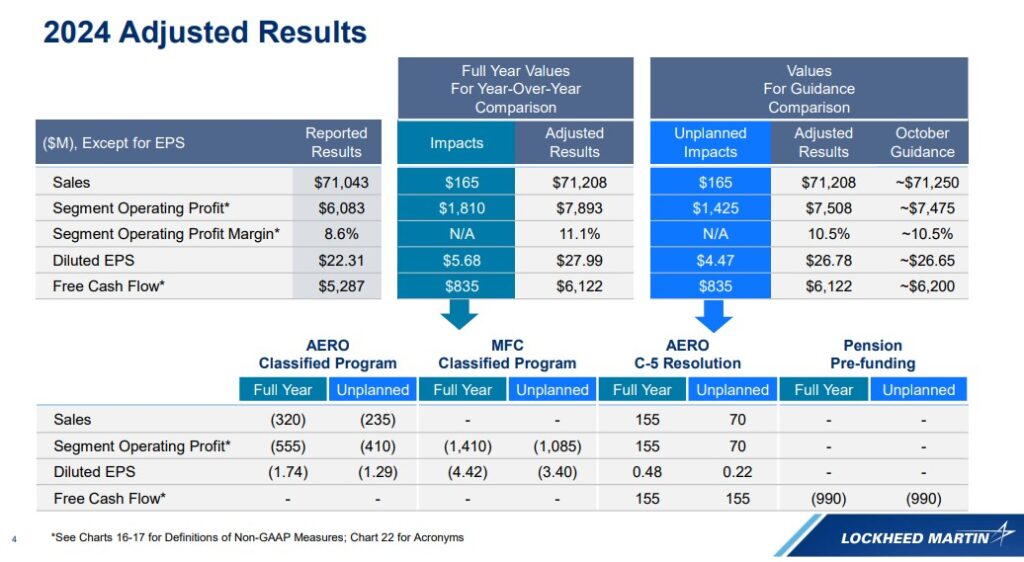

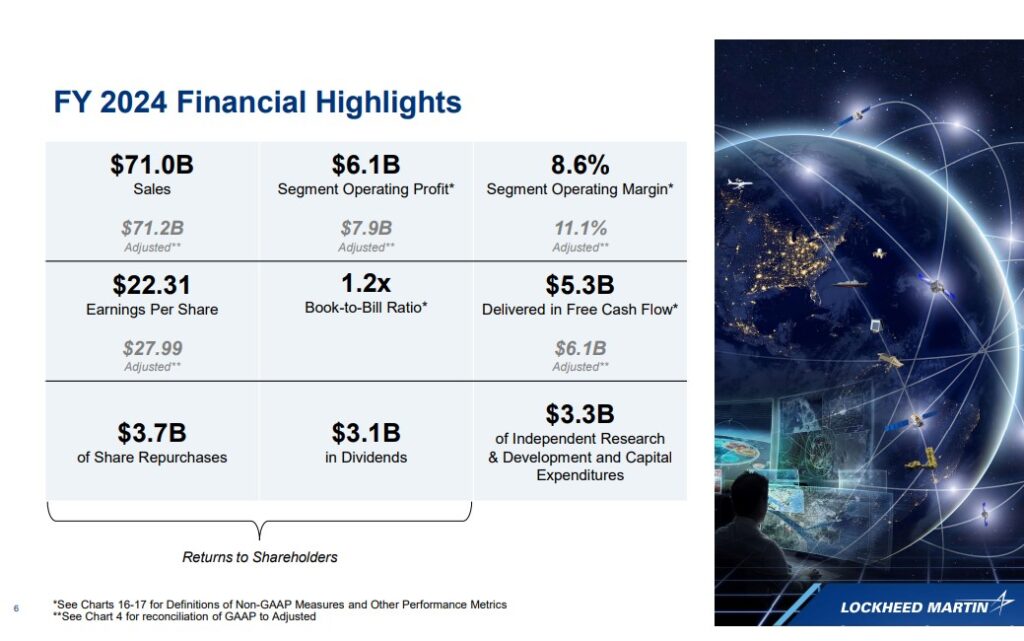

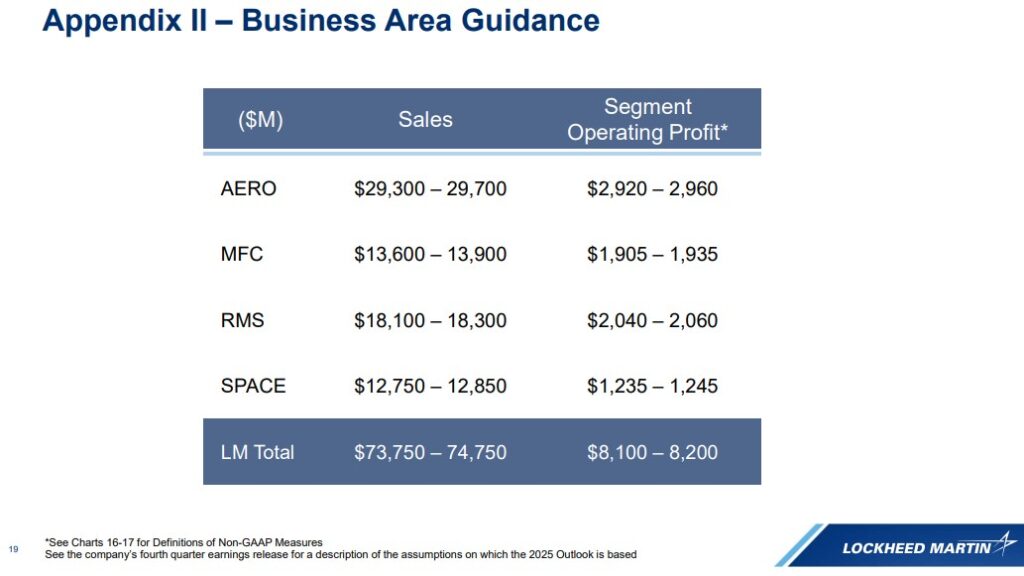

The following images reflect the highlights for LMT as a whole. The Q4 2024 Earnings Presentation, however, provides Sales and Operating Profit results for each of LMT’s 4 business segments.

LMT advanced strategic and technical and operational capabilities by investing over $1.1B in Q4 toward independent R&D and CAPEX projects, bringing full-year internal investment to $3.3B.

From a capital allocation perspective, the financial focus remains on free cash flow (FCF) and FCF/share.

In the second half of 2024, LMT held extensive negotiations with the US military over future F-35 orders AND rolled out major software upgrades to the F-35 fleet. It is now in process of catching up on the delivery of over 400 jets on backorder.

**While the FY2024 financial highlights reflect a 1.2x book-to-bill ratio, LMT recorded over $29B of orders in Q4 for a book-to-bill ratio of ~1.6x.**

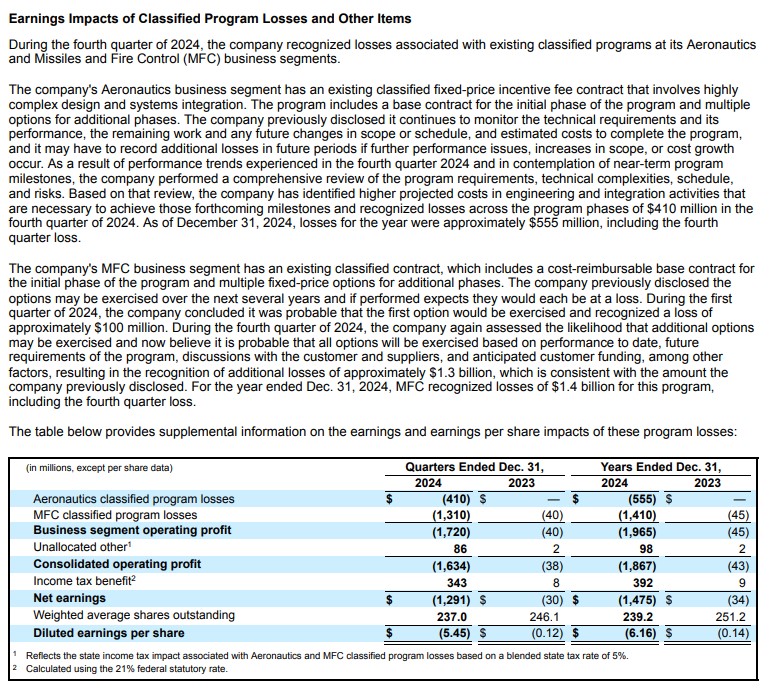

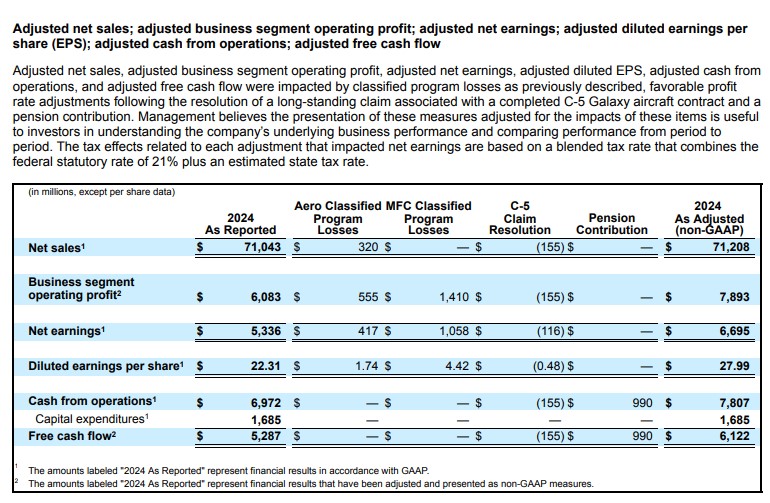

Earnings Impacts of Classified Program Losses and Other Items

LMT’s Q4 and FY2024 results are messy.

- It made a ~$990B pension contribution in Q4 2024.

- Q4 2024 was 13 weeks versus 14 weeks in 2023.

LMT, and its peers, have a few fixed-price contracts that are underperforming as a result of post-covid supply chain cost growth and engineering challenges. The underperformance on these contracts has led to ~$1.965B in classified program losses in FY2024 versus $0.45B in FY2023.

In Q4 alone, LMT recorded net charges of ~$1.72B (~$1.31B related to the remaining expected future losses on the MFC classified program and $0.410B associated with the aeronautics classified program). These amounts are slightly offset by a $0.155B benefit associated with the C5 claim resolution.

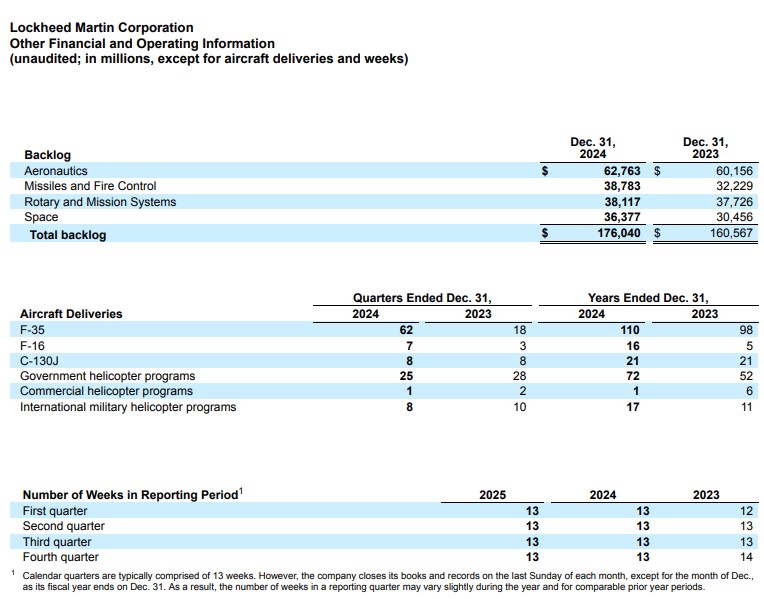

Order Backlog

The following reflect the deliveries and backlog for FY2021 – FY2024.

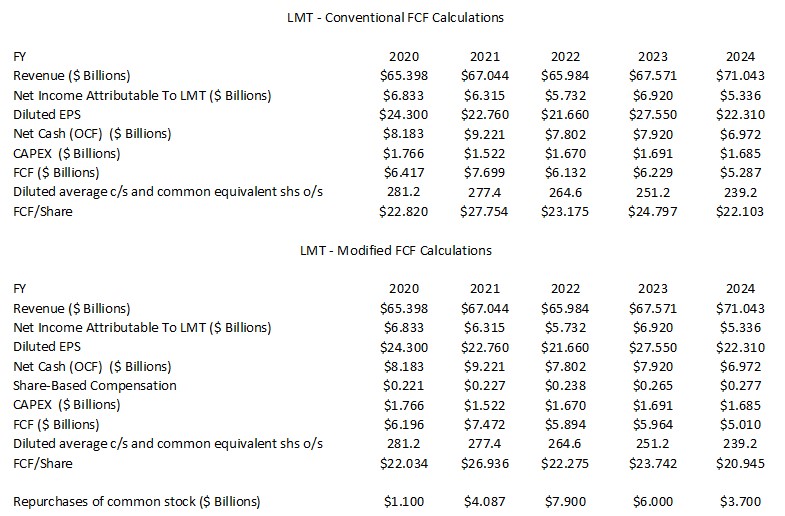

Conventional And Modified Free Cash Flow (FCF) Calculations (FY2020 – FY2024)

In several previous posts I touch upon why I am now taking a conservative approach when looking at a company’s FCF.

FCF is a non-GAAP measure, and therefore, the manner in which we compute it is subject to debate. Most companies subtract capital expenditures (CAPEX) from Net Cash Provided by Operating Activities found in the Consolidated Statement of Cash Flows. As explained in several prior recent posts, I think we need to look at FCF using the conventional method AND a modified method; the modified method also deducts share-based compensation (SBC).

LMT’s FCF/share in FY2023 and FY2024 is ~$1.055 and ~$1.158 lower under the modified calculation versus the conventional calculation.

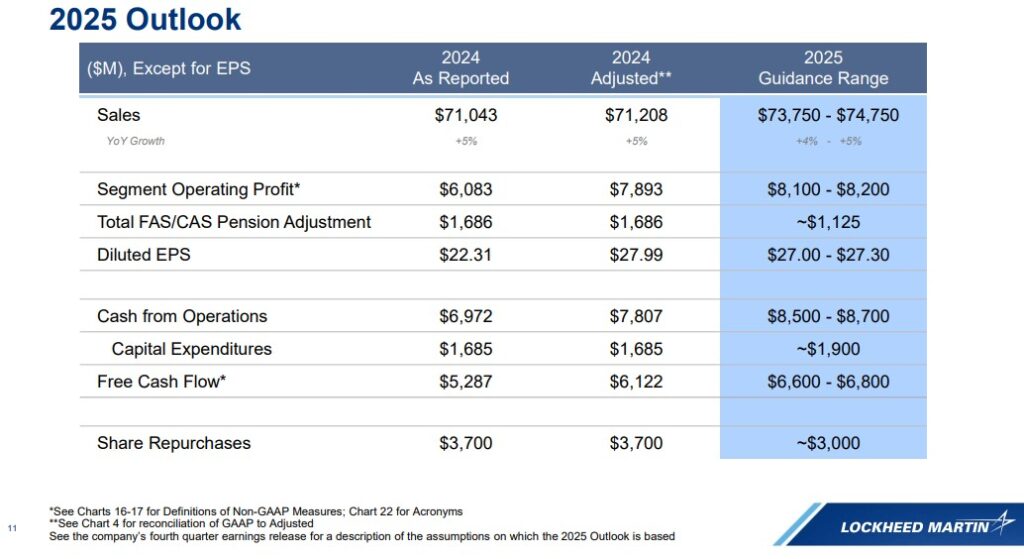

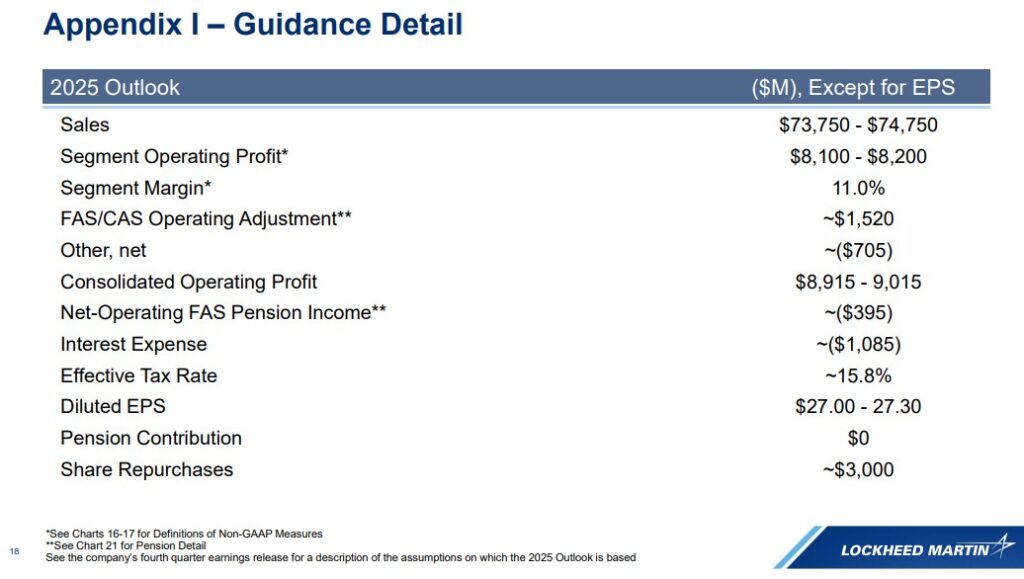

FY2025 Outlook

This is LMT’s current FY2025 outlook.

The following reflect more detail about LMT’s FY2025 outlook.

Risk Assessment

LMT’s senior unsecured domestic currency debt ratings remain the same as at the time of my last review:

- Moody’s: A2 (upgrade from A3 on August 14, 2023 with stable outlook)

- S&P Global: A- (assigned on May 22, 2024 with a stable outlook)

- Fitch: A (upgrade from A- on June 3, 2024 with a stable outlook)

The rating assigned by S&P Global is the lowest tier of the upper-medium investment grade level; the rating assigned by Moody’s and Fitch is one tier higher.

All 3 ratings define LMT as having a STRONG capacity to meet its financial commitments. LMT is, however, somewhat more susceptible to the adverse effects of changes in circumstances and economic conditions than obligors in higher-rated categories.

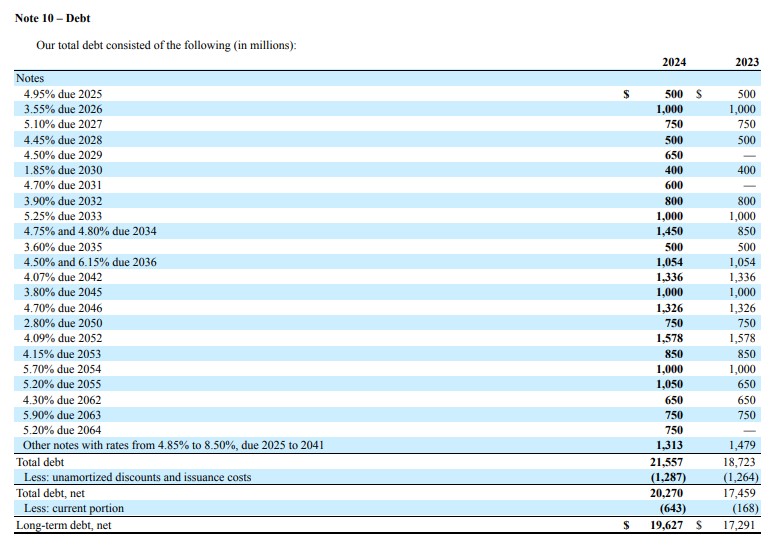

In addition to looking at a company’s credit ratings, I want to know the breakdown of a company’s debt. Details of LMT’s debt is in Note 10 of the FY2024 Form 10-K starting on page 81 of 133. The Form 10-K is accessible through the SEC Filings section of the company’s website.

Dividend and Dividend Yield

LMT has increased its dividend for 22 consecutive years; its dividend history is accessible here.

On January 28, LMT’s Board authorized a Q1 2025 dividend of $3.30/share. It is payable on March 28, 2025 to holders of record as of the close of business on March 3, 2025.

LMT is a prolific acquirer of its shares. The weighted average number of shares was ~340 million in FY2011 versus ~237 million in Q4 2024.

In FY2023 and FY2024, LMT repurchased $6B and $3.7B of its issued and outstanding shares.

The FY2024 outlook includes the repurchase of ~$3B of outstanding shares.

Valuation

I thought LMT was overvalued at ~$511 when I wrote my July 24, 2024 post. The share price, however, marched higher to a ~$619 52-week high in October 2024. I don’t know what would have possessed anyone to acquire shares at that level but with a pullback to $457.75, I view LMT’s valuation as appealing thus prompting me to acquire 50 more shares.

In FY2024, LMT generated ~$22.31 and ~$27.99 of diluted EPS and adjusted diluted EPS. Based on my purchase price, the trailing PE is ~20.5 and ~16.35, respectively.

Management’s FY2025 adjusted diluted EPS guidance is $27 – $27.30. Using the $27.15 mid-point, the forward adjusted diluted PE is ~16.9.

Current broker guidance will change over the next several days. The forward adjusted diluted PE levels using current estimates, however, are:

- FY2025 – 22 brokers – mean of $27.74 and low/high of $26.75 – $29.20. Using the current mean, the forward adjusted diluted PE was ~16.5.

- FY2026 – 18 brokers – mean of $29.82 and low/high of $28.50 – $31.40. Using the current mean, the forward adjusted diluted PE was ~15.4.

- FY2027 – 10 brokers – mean of $31.55 and low/high of $28.77 – $34.27. Using the current mean, the forward adjusted diluted PE was ~14.5.

- FY2028 – 2 brokers – mean of $32.83 and low/high of $31.19 – $34.46. Using the current mean, the forward adjusted diluted PE was ~14.

Using LMT’s FY2024 $22.103 conventional and $20.945 modified FCF levels, the P/FCF is ~20.7 and ~21.9.

LMT’s FY2025 FCF outlook is ~$6.7B. If we deduct ~$0.27B in new shares issued under its various SBC programs, the modified FCF is lowered to ~$6.43B.

LMT intends to repurchase $3B of shares in FY2025. The average purchase price and the timing of the purchases will naturally impact the diluted weighted average number of outstanding shares. If it repurchases shares at an average price of $500 in 2025, this amounts to 5.4 million shares. LMT, however, will issue new shares under its various SBC programs. In Q4 2024, the weighted average was 237 million shares. It does not seem unreasonable to envision a FY2025 weighted average of 234 million shares. Based on this, FCF/share under the conventional and modified methods of calculating FCF should be:

- ~$6.7B/234 million shares = ~$29

- ~$6.43B/234 million shares = ~$27

Divide my $457.75 purchase price by these FCF/share estimates and we get P/FCF values of ~15.8 and ~17.

Final Thoughts

In Q4, LMT recorded ~$1.72B in classified program losses in 2 of its business segments; LMT previously disclosed risks on fixed price classified programs in its portfolio. The investment community, however, was probably not expecting LMT to recognize such large one-time charges all in one quarter. The company’s decision to do so is undoubtedly affecting share price behavior.

LMT’s annual revenue is less than $75B yet the US government spends close to $900B on military and defense. It is not surprising, therefore, to expect an evolution of the aerospace and defense industry with new entrants vying for a ‘slice of the pie’.

The newly-created Department of Government Efficiency (DOGE) will undoubtedly shake up the industry but to what extent is subject to debate.

Acquiring shares in late 2024 was foolish considering LMT’s fair value appears to be closer to ~$520. At $457.75, I envision a ~13% – ~14% return (($520 – $457.75)/$457.75) if LMT’s share price improves to ~$520. Given this potential return, I view the current share price weakness as a buying opportunity.

I wish you much success on your journey to financial freedom!

Note: Please send any feedback, corrections, or questions to [email protected].

Disclosure: I am long LMT and RTX.

Disclaimer: I do not know your circumstances and do not provide individualized advice or recommendations. I encourage you to make investment decisions by conducting your own research and due diligence. Consult your financial advisor about your specific situation. I wrote this article myself and it expresses my own opinions. I do not receive compensation for it and have no business relationship with any company mentioned in this article.