We’re delighted to share this month’s executive summary from Future Horizons’ February report on the semiconductor market, which includes the latest industry insights and projections.

Executive Summary

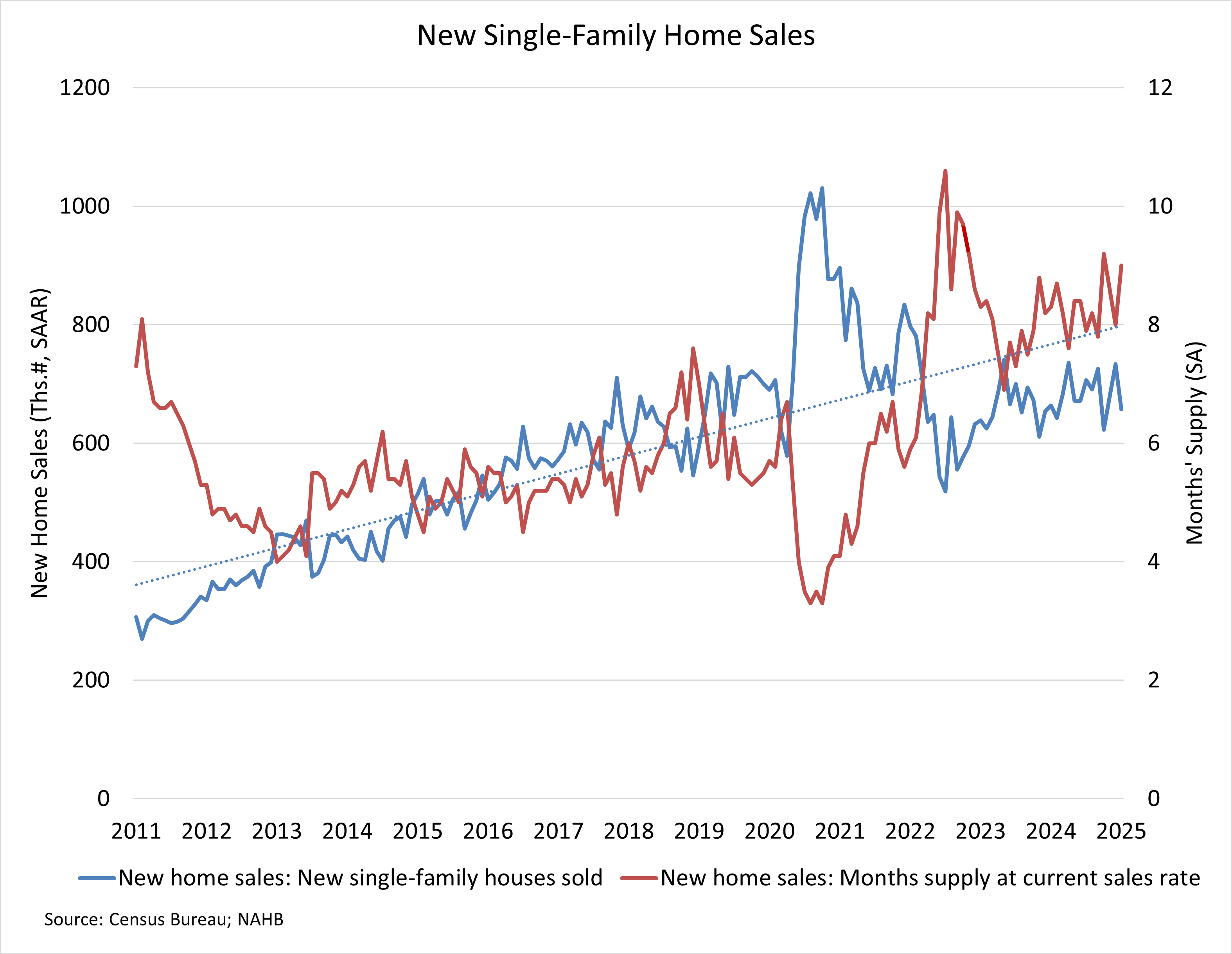

Annualised growth rates fell back in December, with Total Semiconductors growing 14.5 percent, down from 22.2 percent in November, led by Total Memory, at 37.7 percent, a sharp reduction from November’s 87.2 percent number.

Logic growth was flat, at 19.4 percent, with Analog ICs at 2.5 percent, a much welcomed, if small, improvement on November’s 0.6 percent number.

Total Micro performed worse, chalking up a 1.6 percent decline vs. last month’s 1.0 percent lacklustre growth, bringing Total IC growth to 18.6 percent, or 10.7 percent excluding Memory, down from last month’s 22.2 percent and 11.2 percent respective results.

The monthly year-on-year annualised growth rates, which peaked in 28.0 percent in August 2024, have been falling now for four months in a row, Figure E1(a). We do not expect this trend to reverse anytime soon.

Following the euphoria of 2024’s AI-Hyperscale growth, the real market reality is now coming to the fore. Quite where the average 2025 growth rate ends up will be determined by how fast and by how much the ensuing monthly annualised growth rates will fall.

As can be seen from the 2021 to 2023 transition path, correctly guessing this number right is more lucky than good judgement.

Total month-on-month Semiconductor sales were 9.3 percent lower than November 2024, reversing November’s 10.3 percent growth. This decline was broadly spread across all IC sectors, as well as Total Opto, with Total Discretes the only product growth area, at 3.9 percent.

With growth wholly dependent on one market, namely AI infrastructure, even a minor misstep here would have dramatic ramifications for the overall chip industry. Right now, however, the AI frenzy shows no signs yet of abating, with the four big tech firms, Alphabet, Amazon, Microsoft and Meta all doubling down on their infrastructure investments.

This unbridled enthusiasm is, however, starting to see some pockets of scepticism and investor concern, as shareholders worry that doubling down on spending, without a commensurate increase in revenues, would starve non-AI business lines and eat into capital that would otherwise be returned to them as share buybacks and dividends.

Few people doubt AI is potentially game-changing but, correctly in our view, only if AI addresses a clear problem that needs a 10x advantage; has clean data to process; and overall compute costs decline dramatically.

Providing ChatGPT or GenAI features to search engines or MS Office only adds incremental value, it is neither disruptive nor game changing. As such, it offers little potential, if any, for increased revenue generation. It simply provides more bang for the same buck, one of the key fundamental hypotheses that has driven the industry since time immemorial.

If investor patience runs out, any pause or slowdown in the current AI infrastructure spend would trigger an immediate and dire bullwhip oversupply situation. From today’s undersupply backdrop, be it nVIDIA GPUs, SK-Hynix’s HBW memories, or TSMC’s CoWoS packaging, long backlogs and delivery times would be reined back dramatically, there is never a nice smooth inflection and no advanced warning.

Given the overall weak global economic outlook, the increased political uncertainties, and the risk of an AI data centre investment slowdown, following two years of hypergrowth, we do not expect to see the real semiconductor rebound before the second half of 2025 at the earliest.

Overall, we remain committed in our view that the more normal aspects of the market, now in their ninth quarter of recession, have yet to recover.

If the AI market implodes, even a recovery here would not be enough to save the chip market.

There is now a real danger 2025’s growth will go negative.

Read The Full Report Here: https://www.futurehorizons.com/page/137/